Facing high long term care cost is a nightmare everyone wants to avoid, particularly baby boomers. America’s baby boomers have reached its greatest height with 76 million entering their retirement years and 70% of them will require some form of long term care.

Unfortunately, most baby boomers are not prepared to pay for long term care, which isn’t covered by Medicare or health insurance. In effect, they might end up exhausting their retirement nest egg or worse they become a financial liability to their loved ones.

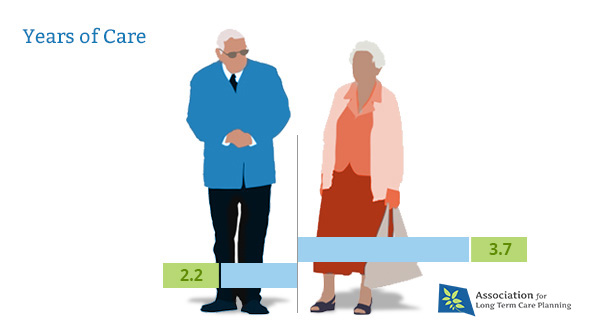

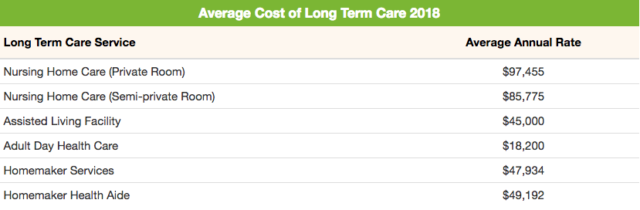

The average cost of a private room in a nursing home is $100,379 annually and the average length of time individuals would need long term care is about two to three years.

Did you know: the average length of stay in an assisted living facility is 2.5 to 3 years and the average length of stay in a nursing home is 835 days or more than two years.

According to a study by the U.S Department of Health and Human Services, it is projected that 48% of individuals who are turning 65 between 2015 and 2019 won’t need paid care. But more than one-fourth will need more than $100,000 of care and 15% will need care that costs more than $250,000. The bill could top $500,000 over five years for an individual with Dementia in a memory-care unit in a nursing home.

To quote Jean Young of the Vanguard Center for Investor Research and co-author of a study analyzing health care costs in retirement.

That’s why it’s important to assess the risks. The study concludes, “Even if the probability of incurring expensive care is relatively low, the number is at a magnitude that is hard to ignore.”

Baby Boomers Should Personalize the Risk

Since the cost of care varies from one person to another, it’s recommended to determine your needs first, the type of care you need, cost of care in your area, your savings and how you can incorporate your long term care expenses in your financial plan.

To help you get started, here’s the latest cost of long term care today.

Check out our interactive map to learn about long term care cost in different states.

You can also answer this short long term care quiz to help you jumpstart your long term care plan.

Explore Long Term Care Payment Options

1. Self-insuring

It’s possible to self-insure if you have at least $2 million as retirement savings. Here’s how you can do it:

- Work with a financial advisor that can help you determine how much you might need to cover your potential long term care expenses. Working with a financial advisor is recommended to help you assess if you’re on track to reach your goals.

- Mix your investments. You should separate your long term care funds from retirement assets. It makes sense to have a relatively aggressive investment mix if you don’t expect to need long term care for some time. If you don’t plan to touch it for 20 years, you can opt for more aggressive investments such as equities. But as you get older, you need to change your strategy and consider making conservative investments instead.

- Consider opening a Health Savings Account or HSA. An HSA is a good place to put your long term care savings. The money that goes into your account is on a pre-tax basis and withdrawals can be tax-free if you use it to fund your long term care.

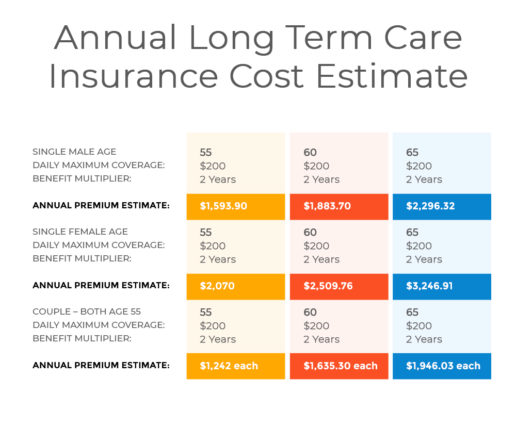

2. Long Term Care Insurance

Long term care insurance is the best option for people who cannot self-insure but has more than $300,000 – the limit to be eligible for Medicaid. This type of policy helps fund long term care services and facilities that you might need because of old age, illness or injury.

Buying long term care insurance early when you’re in your 50s is recommended to avail preferred health discounts. If you delay getting coverage, you might end up getting high premiums or you will be denied of coverage because of pre-existing conditions.

Having coverage is not just beneficial for the policyholders since it also protects their loved ones from stressful caregiving duties or devastating long term care costs.

3. Medicaid

Medicaid can be used to pay for long term care but you need to be eligible first in to enjoy the benefits. Medicaid eligibility depends on assets and financial resources. Some states impose a limit of $3,000 to become eligible for Medicaid. But take note that the eligibility limit varies from one state to another.

4. Hybrid Policy

A hybrid policy or life insurance with long term care rider provides more benefits, which makes it very attractive. It provides both death benefit and long term care benefit. This is perfect for individuals who want to leave a legacy to their loved ones and at the same time would need some long term care.

But this type of policy has downsides. Aside from paying huge premiums upfront, its long term care benefit is also limited, which is risky considering the high cost of care today.

Final Word for Baby Boomers

Baby boomers should focus on financing their potential long term care needs as they make plans for their future. It’s a huge expense that they shouldn’t leave unnoticed even if the need for long term care is still in the distant future. They need to address it early for their financial security and also to protect the people they love.

One thought on “How Aging Baby Boomers Can Address the High Cost of Long Term Care”