Are you still in limbo whether you should buy long term care insurance before age 50?

Better make up your mind now and buy coverage to avoid paying for expensive long term care cost out-of-the-pocket. It’s hard to fathom the financial strain of long term care now, but by looking at the latest cost of care survey by ALTCP and taking into consideration your high chance of requiring any form of care, you’ll get an idea of what you’re future would look like. But, you haven’t planned for that expense.

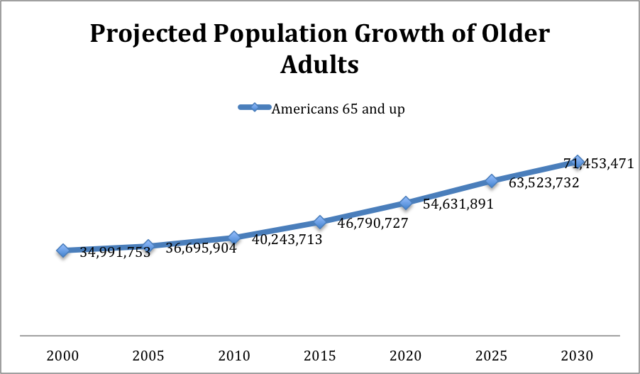

There are only roughly 7.2 million Americans who have long term health care insurance, which pays for nursing homes, assisted living facilities, adult day care, CCRCs – long term care facilities not covered by Medicare. If you look at the projected population growth of older adults today, a lot of people are at risk of requiring long term care, but only a few people purchased coverage.

Every year you delay getting insurance, will make it more expensive and makes you highly at risk of emptying your nest egg just to cover your expenses. Better shop for the lowest prices from top companies now to save time and increase your savings when buying coverage.

Here are the things need to know why you should stop putting off getting coverage.

Top Reasons Why You Should Buy Long Term Care Insurance Before Age 50

1. Protect your Savings

Have you ever imagined that everything you’ve worked hard for could just disappear because of long term care?

With the way the cost of long term care is increasing today, there’s a big possibility that your savings will get wiped out. To add insult to injury, you can become a burden to your loved ones – physically, financially and emotionally.

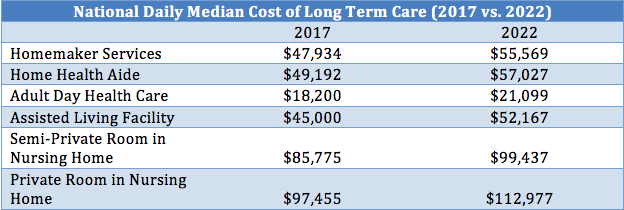

To give you an idea of the cost of long term care today, here’s a table of the average daily cost of care and their projected cost in five years.

The average length of staying in a nursing home and assisted living facility is around 835 days, which would cost you hundreds of thousands of dollars. Instead of paying out-of-the-pocket, your long term health care insurance will pay for your care expenses.

Read: Protecting Assets from Nursing Home Costs in 6 Ways

2. Enjoy Lower Premiums

The younger and healthier you are when you apply for a policy, the lower your premiums will be. Despite this, most Americans still choose not to get covered because of false assumptions that their savings will be enough to cover the cost of care or they will not receive care later in life.

According to Bankrate’s latest financial security index survey, most Americans don’t have enough savings to pay for a $1,000 unexpected expense like long term care. Those who can’t pay the cost from their savings would resort to other ways to cover that expense, 19% their credit card, 13% of them would reduce to spend on other things, 12% would borrow from friends, and 5% would take out a personal loan.

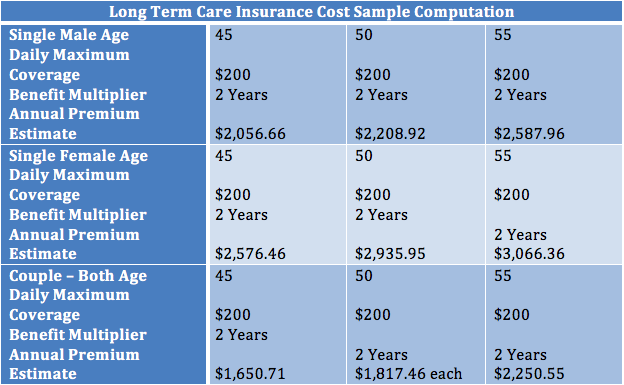

Save yourself from the trouble of exhausting your savings or borrowing money just to cover your long term care needs by getting coverage. Besides, this option is cheaper by miles than to pay out-of-the-pocket. Here’s a sample computation of the cost of long term care insurance when you buy early.

Read: Facing Long Term Care Insurance Rate Hikes

3. Avoid Rejection of Long Term Health Care Policy Application

Delaying buying long term health care insurance might result in getting disqualified for coverage. Declined applications are rampant among older applications. Around 45% of applicants 70-79 are denied coverage due to health issues. While 17% of applicants 50-59 are also denied because of poor health.

However, underwriting guidelines differ from one insurer to another. Some insurers might decline certain conditions while others might consider it. So, don’t wait until you’re older and it’s too late for you to get covered. Do it now while you’re still healthy and can qualify for coverage.

Here are some of the pre-existing conditions and reasons why applicants are denied coverage.

- Needing assistance in ADLs or activities of daily living such as bathing, eating, dressing, transferring to a bed or chair or toileting.

- Receiving care at home or staying at adult day care, nursing home, or facility care services.

- Currently receiving narcotic pain medication.

- Using walker, wheelchair, quad cane, motorized scooter, nebulizer, ventilator, hospital bed, oxygen, or kidney dialysis.

- Currently in physical therapy.

- Receiving disability benefits.

- AIDS/HIV+

- Alzheimer’s

- Amputation due to disease

- Amyotrophic Lateral Sclerosis (ALS or Lou Gehrig’s Disease)

- Cancer of bone, brain, esophagus, liver, pancreas, stomach

- Cirrhosis of the liver

- Congestive Heart Failure (CHF)

- Cystic Fibrosis

- Dementia

- Frequent/Persistent forgetfulness or memory loss

- Huntington’s Chorea

- Chronic Kidney Disease

- Metastatic Cancer (spread from original site)

- Multiple Sclerosis

- Muscular Dystrophy

- Organ Transplant other than kidney or cornea

- Organic Brain Syndrome

- Paralysis

- Parkinson’s Disease

- Scleroderma

- Schizophrenia or other forms of Psychosis

- Systemic Lupus

- Transient Ischemic Attack (TIA) within two years or more an one TIA

4. Relieve Burden on Family

There are approximately 43.5 million caregivers that have provided unpaid care. A lot of people stay home and receive care from their loved ones because they can’t afford the cost of a home health aide or a long term care facility.

While it is a fulfilling task, family caregivers also have other responsibilities to attend to like their job, children, household chores and more. In effect, caregiving takes a toll on their mental, physical and financial health.

Here are some negative effects of caregiving on your loved ones.

- 1 in 5 of caregivers experiences high levels of physical strain.

- 1 in 5 of caregivers experiences financial problems.

- 2 in 5 caregivers experience emotional stress.

- 3 in 5 caregivers with jobs have experienced at least one impact in their employment situation.

Spare your loved ones from the expensive cost of long term care by planning and getting coverage early.

Read: 18 Enlightening Facts about Caregivers

5. To Have Peace of Mind

Long term health care insurance gives you peace of mind, at a price. A price that is worth it since it helps you combat the fear of being vulnerable to growing old and succumbing to conditions and diseases, financial independence and as well as senior-living stereotypes.

There’s not a single day you’ll think about how you would pay for care since this coverage pays for different types of long term care facilities. You can just sit back, make the most of your time with your family and enjoy retirement just like how you imagined it to be.

One thought on “Why You Should Buy Long Term Care Insurance Before Age 50”