Insurance policies are one of the most overlooked financial products today.

Why?

People don’t buy insurance because they think they wouldn’t need it, not now or not in the near future. But without coverage, you could be one accident, disease, house fire or car crash away from succumbing to debt.

You don’t have to buy all kinds of insurance but there are certain types of insurance that should be on your radar by now. The key is determining policies that could give you maximum protection and can help preserve your retirement savings, and find a seamless way to include it in your financial plan.

Here are types of insurance policies ALTCP recommends:

Life Insurance

Life insurance is not exclusive to people who are married or those with children. People who are single can also benefit from life insurance. In the case of the former, this type of policy can help pay for debts like mortgage after the death of the policyholder or can be used to fund college education and other financial obligations In the case of the latter; life insurance can pay for debts or burial costs.

If you don’t have one yet, consider getting life insurance now through your employer or through an insurance broker you trust.

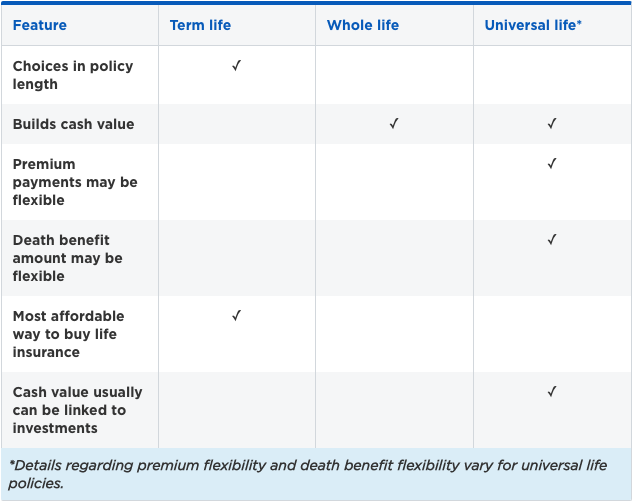

Not sure what type of life insurance to buy?

Here is a comparison chart of different types of life insurance.

Credit: www.nerdwallet.com

Long Term Care Insurance

Long term care insurance provides optimum protection to people who will need assistance in carrying out their activities of daily living (ADLs) like eating, bathing and walking for an extended period. Long term care services are expensive and to make things worse, these are not covered by Medicare and Medicaid.

Here is a chart of the current average cost of long term care

So who should buy long term care insurance?

You will not likely need this now but think about your current health and family history. Consider these two factors when buying long term care insurance. Moreover, it’s also important to consider buying at a younger age to take advantage of lower premiums.

You may not be close to the best age to buy long term care insurance, but your loved ones might be, so find time to explore long term care and long term care insurance through this long term care planning tool.

Health Insurance

The rising cost of medical cost is one of the reasons why people outlive their retirement funds. A simple visit to the family physician can generate a hefty bill what more if you’ll develop conditions or diseases that would require hospitalization that could quickly rack up a five-figure bill.

Make sure to compare health insurance policies first to find what’s best for your future health care needs.

Credit: www.nerdwallet.com

Car Insurance

Never drive without car insurance. But not only for the purpose of adhering to the law of certain states that require having basic auto insurance but also to protect yourself from costly liabilities.

Here are the different car insurance options you can choose from:

- Comprehensive coverage – This type of insurance policy provides coverage for your losses that are not caused by flood, fire, vandalism, and theft.

- Collision coverage – This policy pays for the cost of repair or replaces your home if it is damaged or destroyed.

- Liability coverage – This type of coverage will cover the cost of property damages, injuries caused by the collision if you’re at fault for the accident.

Homeowners Insurance/Rentals Insurance

One of the biggest assets you have is your home. If you don’t take care of it and protect it from damages, then it will cost you a lot of money in the long run. That’s why it is important to have home insurance. This can help pay for home repairs, short-term lodging in case you will not be able to live in your home while repairs are made and a new home.

It’s important to double-check what your policy covers and what it doesn’t. Here are some of the things you should look into when buying homeowners insurance:

- Extended dwelling coverage – This provides an additional layer of protection above the limits of your policy. Your policy will repair or replace your property even if the cost exceeds the coverage of your policy. They will only shoulder 20-25% above the amount you are insured for unless you will opt for additional coverage.

- Earthquake coverage – Ask your agent if this is included in your policy because this coverage depends on the state you live in.

- Flood Insurance – Flood insurance is excluded from homeowners insurance, and this is also different from water backup protection. If you have questions regarding this coverage, ask your broker to give you more details about this.

Umbrella Policy

If you want to have an additional layer of protection for you and your assets in case you’ll go over the limit of your auto insurance or homeowners insurance, then you should get this type of insurance policy.

This is recommended for people who have a net worth of $500,000 or more. An umbrella policy can increase your coverage from $500,000 to $1.5 million if you shell out a few hundred dollars annually.

Disability Insurance

The odds are too high if you opt not to get disability insurance.

Why?

According to the Social Security Administration, around 1 in 4 of 20-year-olds will become disabled before they reach the age of 67. So it is important to have long-term disability insurance, to protect you from the loss of income in case you can’t work for an extended period because of an injury or illness.

You don’t want injuries or diseases to shatter your dreams of having a flourishing career, a comfortable life, your own house and paying for your children’s education.