Long term care insurance helps in securing your future and protecting your family from the exorbitant cost of nursing homes, assisted living facilities and other forms of long term care. But nothing is more important than applying for long term care insurance claims, getting approved and using all your benefits.

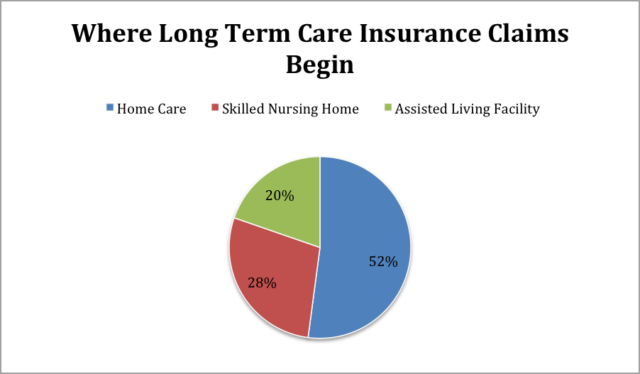

According to this article by McKnights, long term care insurance companies paid $9.2 billion in claim benefits to 295,000 policyholders in 2017. More than half of new claims to long term care insurance started at home. Here’s a figure of where new long term care insurance claims began last year.

Filing a claim for your long term care insurance entails a process you need to follow and you also need to know the important requirements needed to get your claim application approved. It may seem daunting to file for claims but in fact, it can be done swiftly as long as you follow the steps accordingly.

In fact, according to a survey by AHIP, from 64% of policyholders that claimed that filing for claims easy in 2005, it rose to almost 80% today. This shows that the long term care insurance claim process is constantly improving.

To make the claims process easier, we came up with a complete and easy to understand steps when filing for claims.

Steps When Filing for Long Term Care Insurance Claims

1. Review your Policy

Read your entire policy first before you initiate the claims process and contact your insurer. Review everything that is included in your policy and pay attention to long term care insurance features such as the benefit for different types of long term care settings and services, total benefit pool, benefit period and elimination period.

2. Understanding Benefit Triggers

If you’ve visited our FAQ page, you can find a brief description of how does long term care insurance work. Long term care insurance only starts paying benefits when you can no longer do at least two of ADLs and you are beyond the elimination period stated in your policy.

Benefit triggers are defined as qualifying events to become eligible to claim your policy benefits. You can trigger your benefits when you can no longer perform at least two of the six ADLs – eating, bathing, dressing, toileting, incontinence and transferring or you have a severe cognitive condition such as Alzheimer’s or Dementia.

3. Understanding Elimination Period

The elimination period is described as the timeframe or period you need to wait before your long term care insurance begins paying benefits. This waiting period begins as soon as you trigger your benefits. Most long term care insurance companies offer 30, 60 or 90 days elimination period. This means you have to pay for long term care costs out-of-the-pocket first before your policy kicks in.

Once you know your policy’s elimination period, you need to find out how the days are counted against it. An elimination period based on calendar days will deduct days you’ve been waiting starting from the date you triggered your benefits regardless if there are days you didn’t receive care. So, if the elimination period of your policy is based on calendar days, your insurer will begin paying claims after your benefits are triggered.

In case your policy is based on service days, your insurer counts the number of days you received care. If you have a 90-day elimination period and you only received 4 days of care in one week, your elimination period can extend by more than 3 months.

4. Determine the Care Providers your Policy Covers

Long term care insurance pays for different types of long term care facilities and services. However, not all policies are the same. There are some policies that pay for nursing homes while there are other policies that pay for nursing home and in-home care.

Review your policy first and find out what your policy covers. If your policy pays for in-home care find out if it pays for care provided by a loved one because there are some policies that only pay for licensed caregivers.

5. Contact your Insurance Company

You don’t need to wait for your elimination period to be over before contacting your insurer. Get in touch with your long term care insurance provider to initiate the claims process.

Your insurer will give you instructions on how to file for a long term care insurance claim. You need to fill up a long term care insurance claim form and submit requirements from your physician and the plan of care from your provider. Take note that requirements vary from one insurer to another.

If your policy covers care coordinator services, it’s recommended to take advantage of this to help you create a care plan and in the claims process as well.

6. Submit All Requirements

Submit all the information and requirements needed to start your claim process such as fully accomplished claim form, certification from your physician that the care treatment you receive is due to a medical condition or a record of the type of care you are receiving. Your insurer will use the said documents to determine whether you are eligible for long term care insurance benefits.

In addition to these documents, your insurer might require you to submit other documents such as receipts of all your long term care expenses before your insurer starts paying benefits. So, make sure to keep all receipts, paperwork or any record related to your care needs.

7. Assessment of Insurance Company

After filing your long term care insurance claim, your insurance company will validate all the requirements you submitted and determine if you’re eligible for benefits.

Insurers usually interview claimants through a visit by their nurse or through a phone call. The extent of your long term care needs will be determined based on your physical and cognitive abilities.

You will not encounter any problem receiving your benefits once your insurance provider finds the requirements you submitted and the result of their assessment sufficient to prove your claim.

In case your insurance company finds that you are not eligible for long term care insurance benefits, you will receive a letter stating the reasons why they denied your claim.

Read: What Does Long Term Care Insurance Cover?

What Can I Do if My Long Term Care Insurance Claim is Denied?

If you receive a denial letter from your insurer, you can file an appeal and in the end, you might still be able to receive benefits.

Here are things you can do in case your insurer denies your long term care insurance claim.

1. Compile all the documents

Gather all documents related to your claims such as your policy, claim form, certification from your physician, records from your long term care provider, communication log between you and your insurer and denial letter.

2. Review your Documents

Go through all your documents especially your long term care insurance policy to find out if it justifies your insurer’s decision to deny your claim.

3. Consider Hiring a Lawyer

Find a lawyer who specializes in long term care insurance. With the help of a lawyer, you can find out whether the denial is reasonable or if the company acted in bad faith. If the denial is unreasonable, you have a strong case that you should raise to your insurance company right away.

4. Alternate Plan of Care

Explore an alternate plan of care in case your insurer offers this option.