Current estimates show that 70% of individuals aging 65 and above will need care. Meanwhile, 40% of people between the ages of 18 and 64 will require care of some sort. Given these figures, long term care is a need that can befall many, including you. This must have prompted you to start working on acquiring long term care insurance. However, you should get familiar with important long term care insurance problems first before buying coverage.

Long Term Care Insurance Problems and Solutions

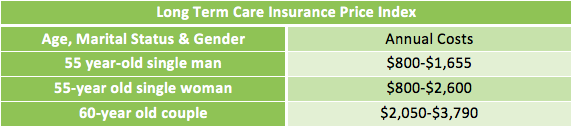

1. Overpayment

If your purchase is not planned thoroughly, you can end up paying more than what you should. This happens when you fail to do comparison shopping and when you signed up for coverage that’s beyond your requirements.

Before buying long term care insurance, be sure to shop around for different rates from different insurers. You can easily do so by requesting long term care insurance quotes online. As you do, make sure that you are doing an apples-to-apples comparison. Meaning, you are looking at two policies that have the same benefits.

More so, make sure that you know what your needs are. Surely, a policy that covers you for life is a comprehensive coverage. However, remember that premiums for such coverage can cost high. The cost-effective way to go about it is to match your benefit duration by how long you’ll likely need care. You can do so by consulting your doctor to see if you are a candidate for certain conditions based on your lifestyle, health records and family’s health background. This will not give you an exact picture. However, evaluation or assessment is better than nothing.

Apart from this, determine how much you can self-insure should your benefits become insufficient for your needs. Shouldering a portion of your care expenses can have implications on your finances. That’s why it’s best to anticipate and prepare for it.

Also Read: 5 Ways to Avoid Overpaying for Long Term Care Insurance

2. Premium Increases

It is encouraged to buy long term care insurance while you’re still young, typically before you turn 50. This is because premiums for younger policyholders are more affordable than those who acquired coverage at an older age. However, buying young doesn’t exempt you from rate increases in the years to come.

Insurers cannot make individual increases, but they can do so on a group basis, typically depending on the age. When you reach a certain age bracket, your premiums could go up because your likelihood of making claims went a few notches higher.

If you received notice that your insurer will raise your rates, you could keep your levels premiums by limiting your coverage. Other features you can downsize are your policy’s benefit duration and daily benefit amount.

Read Next: How to Deal With Long Term Care Insurance Premium Hikes

3. Denied Claims

Denial of claims is one of the worst-case scenarios that a policyholder may face. However, this can be avoided on the onset by being 100% clear on what your long term care insurance covers.

Let’s look at long term care settings for example. Before you go for in-home care, clarify if your policy will pay for it. If it does, determine if it will cover compensation for relatives who provide you with care or if it will only shoulder the fees of a licensed caregiver. By being clear on details like this, you can easily avoid the horrors of having your claims denied.

Keeping track of the necessary paperwork is also essential if you want to claim your benefits quickly. Be organized with the necessary documents that your insurer requires before it to pays off your care expenses. If you’re having difficulty, don’t hesitate to ask for assistance. Typically, you can ask your agent to help you with the claims process, or you can seek the help of a coordinator from your insurance company.

4. Insurance Companies Exiting the Long Term Care Business

Some insurance companies have left the long term care field due to miscalculations and the continuous increase in care costs. If you’re still in the process of acquiring long term care insurance, make sure that you buy from a company that has the financial strength to stay in operation. Opt for an insurer who has the capability to remain established up to the time that you’ll make a claim off your policy, which can be years or decades from now.

Before you deal with potential insurers, make sure that you have thoroughly checked long term care insurance company ratings, company profiles, the number of years in business, claims payment history and customer satisfaction ratings. There are independent agencies that conduct periodic evaluations of insurance companies to come up with ratings. You can use their evaluation results for reference.

Long term care insurance is a good strategy of being protected against care expenses that you may incur in the future. However, it’s essential that you go about its acquisition carefully. Consider the long term care insurance problems above as you formulate your plan to ensure that you get the coverage you deserve.