Ltc insurance is the traditional way of paying for long-term care. But due to the increase in premiums and fears that rates will continue to rise, the insurance industry came up with a new product that attempts to solve the issues of traditional ltc insurance, which is life insurance with ltc rider or hybrid insurance.

Is this new alternative to paying for long-term care better than traditional ltc insurance?

Well, it depends on your needs. Ltc insurance might work well for you but others might be better off with life insurance with ltc rider. To help you figure out what’s the best way to fund long-term care, below you will learn how ltc insurance and life insurance with ltc rider works.

LTC Insurance Explained

What Is LTC Insurance and Who Needs It?

Ltc insurance is a type of policy that helps pay for long term care – nursing homes, assisted living facilities, CCRCs and more. This is designed for people who will require assistance in their ADLs like eating, bathing, dressing, toileting and transferring.

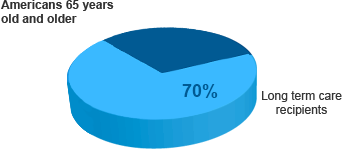

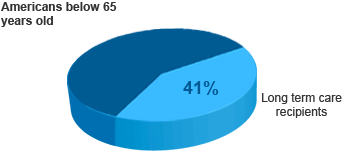

Around 70% of Americans 65 years old and above will require some form of long-term care. In addition to this, around 41% of Americans below 65 years old will require long-term care due to chronic illness, injury from an accident or mental condition.

Should You Buy LTC Insurance?

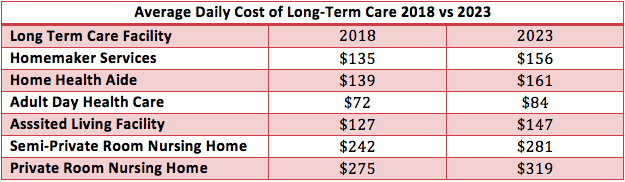

The cost of long-term care continues to rise today, which makes it hard for people to pay for long-term care. Based on ALTCP’s average annual cost of long-term care 2018, the average annual cost of a private room in a nursing home is $100,379 while an assisted living facility has an average annual cost of $46,350. To give you an idea of how expensive long-term care can get, here’s a comparison of ltc costs today and after five years.

Read: The disadvantages of not having insurance for long term care [Infographic]

When Should You Buy LTC Insurance?

The best time to buy ltc insurance is when you’re in your 50’s or when you’re still young and healthy. Buying insurance at this age is wise because of low premiums. Insurers give health discounts up to 10% for potential policyholders because they have a lower risk of requiring long-term care.

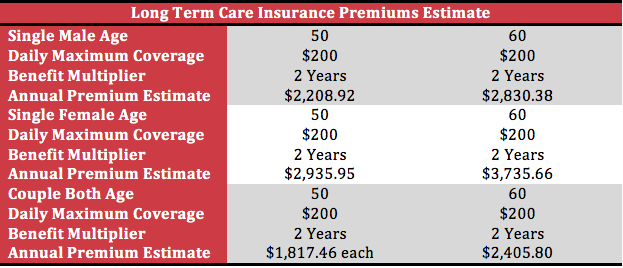

Here’s a sample computation of premiums to give you an idea of the cost of long term care insurance.

One concern that might arise is determining how much insurance you might need since it’s hard to pinpoint the extent of coverage you might need in the future. It would help to have an idea of the average length of stay in long-term care facilities such as nursing homes and assisted living facilities.

Average Length of Stay in Nursing Homes

According to Centers for Disease Control and Prevention, the average length of stay in a nursing home is 835 days or more than two years. But it’s a different story for people suffering from Dementia or Alzheimer’s because they can stay in a nursing home for as long as five years.

Average Length of Stay in Assisted Living Facilities

Based on the 2010 Investment Guide of the National Investment Center (NIC), the average length of stay of residents in assisted living facilities is 29 months or 2.5 to 3 years.

Read: 5 Reasons to Stop Delaying Getting Long Term Health Care Insurance

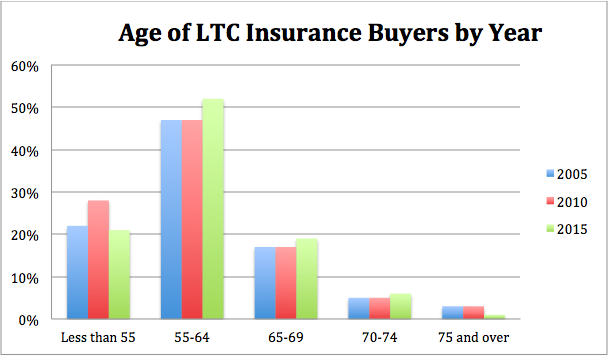

Despite the high risk of requiring long-term care, there are only around 7.2 million Americans who have ltc insurance today, which is alarming. Below you can see the number of ltc insurance buyers by year.

It makes sense to get coverage for long-term care early so you can take advantage of health discounts and also to have peace of mind, knowing that you have funds available for your future long-term care needs.

Delaying getting ltc insurance isn’t wise though because of its negative consequences, to you and your family. So, it’s best to get covered early to have peace of mind that you have enough funds for long-term care.

Understanding Life Insurance with LTC Rider

What is Hybrid Insurance?

Hybrid insurance also referred to as asset-based long-term care provides both living and death benefits. This type of policy is usually used for ltc benefits but they provide tax-free payouts for death benefits.

How Do Life Insurance with LTC Rider Works?

Just like traditional ltc insurance, a hybrid policy offers leveraged payouts, coverage for home care, nursing homes, assisted living facilities and other types of long-term care facilities, inflation protection, and waiting period options. It creates a pool of money that will pay for ltc benefits for a minimum number of years or for a lifetime.

Hybrid insurance policyholders will know their daily or monthly benefit as their policy grows. In case the policyholder will use less than their daily and monthly benefit amount, their policies will last longer than that the designated number of years when they purchased.

Why Should You Buy Hybrid Insurance?

One reason why hybrid insurance is popular today because it provides solutions to issues associated with traditional ltc insurance like premium hikes and paying for coverage that the policyholder might not even use.

Another is its flexibility when it comes to allowing couples joint ownership. This helps couples leverage dollars further assuming that only one spouse will need the majority of the benefits.

This is also a good option for people who have been turned down for ltc insurance because hybrid insurance only requires less underwriting like an application questionnaire and phone interview. There are instances when medical records will be requested but it’s not that often.

However, premiums for hybrid insurance are more expensive compared to traditional insurance for ltc. It is usually funded with a one-time single premium of $50,000 or $100,000.

Comparing Your Options

When comparing ltc insurance vs life insurance with ltc rider, consider your long-term care need. If you have a high risk of requiring long-term care, a hybrid policy may not be the best solution, since you might not get enough coverage for long term care and you’ll end up paying out-of-the-pocket or asking family members to take care of you or for financial help.

Weigh your options carefully by determining your needs first to come up with the best long-term care solution that can protect you and your family in the future.