Money conversations between couples aren’t romantic but these should happen before retirement.

Why?

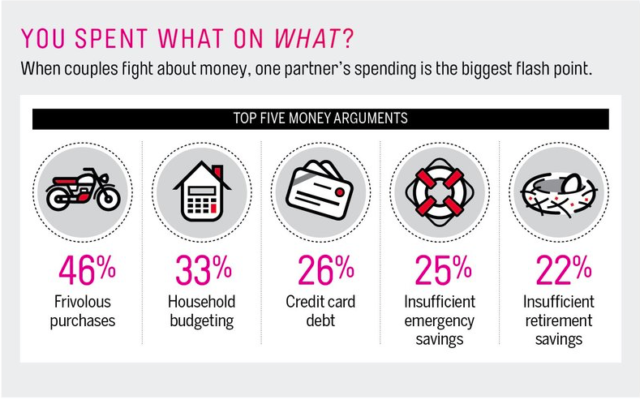

Couples fight about money and most often than not, one spouse’s spending becomes the root of the problem.

credit: www.time.com

Retirement comes with challenges and most of them are deeply rooted in finances like mortgage, utilities, children’s education, debt, savings and one of the most overlooked issue, healthcare and long term care expenses.

It’s best to include long term care in your money conversations now or you’ll end up paying around $97,455 annually for a private room in a nursing home, the current median rate according to Genworth. Explore viable options to cover these expenses like by buying traditional long term care insurance or hybrid policies as early as possible.

It’s important for married couples to be on the same page and to visualize the same things about their future. They should master the art of compromising to maintain a harmonious relationship all throughout their marriage and create a solid retirement plan that will secure their future.

To help you avoid financial woes during retirement, we featured eleven experts to shed light on important money conversations couples should have before retirement.

Money Conversations Couples Should Have Before Retirement

Jillian Montana

http://www.montanamoneyadventures.com

It’s great to start talking about what the ideal day, week or year would look like. “]What will happen each day, what hobbies will you engage in, time with friends, volunteering, or time with family? Then what do you want to make sure happens each week? Or on a yearly basis. Are there big family gatherings? Long trips to see new places, old familiar places, or friends and family?

After you have a good conversation about that over a dinner out, or on a long road trip, you can start planning what will be needed to make those things happen. It’s not all just about money, although that is a factor. What kind of fitness is needed? How do you need to invest in those relationships now to have them strong for retirement? What skills do you need to develop to have meaningful hobbies or volunteer work?

There are lots of ways to lay the foundation for the life you want to live in retirement. But none of it happens by chance. Talking, dreaming, planning and preparing more now will help make the transition seamless and give you the retirement you dreamed about from day one.

Shanna Tingom

https://www.heritagefinancialaz.com

I can’t tell you how often I sit down with couples, some who have been married for decades, and when we talk about retirement, they have VASTLY different ideas on how and where it will be spent. One spouse wants to move to another state, by a loft in the city to be near the kids or grandkids, and the others idea of an ideal retirement is buying an RV and traveling the country! While these dreams may not be mutually exclusive, they do require more financial resources than one or the other. So, I’d say the first question they need to talk about is WHEN and WHERE will retirement take place? What I like to ask clients is “It’s Tuesday at 10:00 am and you’re retired. Where are you, what are you doing and who are you with?”. Make sure the answers are at least compatible.

Emily Jividen

Retirement is a big transition, and sometimes the changes associated aren’t what you expect. You need to think about different phases of retirement, particularly as what you can handle the physical challenges associated with aging.

If one or both of you plan on working some in retirement, you need to discuss those plans, what might change the plans, and what changes might do to your budget.

For instance, right now, my husband and I have rental properties. He does most of the maintenance, which keeps the expenses down. Our early semi-retirement budget is based in part on that income.

What should we do if my husband can’t maintain the properties anymore? Hire out the maintenance and keep the properties with the reduced net income? Or sell the properties and invest the money in the stock market for a more passive income stream? What does each of those decisions do to our budget?

Another issue to think about relates to housing. Do both of you plan on aging in place, or do you plan to downsize? Will you move to a new city or even new country entirely? If you plan on aging in place, can you stay comfortably if your mobility is reduced? What remodels would it take to keep your home comfortable if one or both of you had reduced mobility? What would they cost? Should you do some remodels before you retire to make your home comfortable in retirement?

Ian Myers

- Two must-have money conversations before retirement are framing individual lifestyle expectations and addressing the question of survivorship.

- When it comes to retirement lifestyle, it’s not unusual for partners to have different expectations. Everyone likes to spend their time differently. Instead of assuming what their partners want, spouses should sit down and have a clear, open conversation about lifestyle desires. Then they can start mapping out what their retirement spending will look like and what their monthly income needs will be.

- While an uncomfortable topic, spousal survivorship is too important to leave open-ended. Couples need to have a plan set in case one of them passes away.

- Their plan should create, as much as possible, a comfortable financial transition for the surviving partner. With life expectancies on the rise, it should prepare for the possibility of the surviving spouse living into their 90s in retirement. If a couple worries about outliving their retirement money, they may consider using deferred annuity contracts for a guaranteed, lifelong income stream.

- As we age, cognitive abilities tend to decline, along with our ability to make informed investment and account withdrawal decisions. A survivorship plan must account for the possibility of the surviving partner gradually losing their ability to manage their money well.

- If a couple does consider annuities for their survivorship plan, be careful which annuities they choose. If they go with a joint life annuity and fund it with after-tax money, the surviving spouse may have to start taking required minimum distributions when their partner dies. With a single life annuity, they can potentially avoid taxable missteps like this by naming the partner as a contract beneficiary.

- If a couple will be using retirement accounts as primary income sources, they should be ready ahead of time. Make sure the account owner specifies their partner as a beneficiary on the account. Should the account owner pass away, that enables a more efficient wealth transfer.

- Healthcare and personal care costs will be another factor to include in the survivorship plan. Long-term care insurance can help with managing costly long-term care expenses over time. Medicare doesn’t cover everything, have liquid reserves in place for emergencies like unexpected medical bills. If it makes sense for your portfolio, life insurance policies may come with “living benefits,” or where you can draw on your policy benefits early to pay for healthcare needs.

Experian

Watch and listen carefully to what the panel has to say about this topic: Love and Money: Financial Advice for Couples at Every Stage. The panel includes Vanessa McGrady: Award-winning journalist and Forbes personal finance and prosperity contributor; Tai McNeely: Co-Founder of His & Her Money, America’s #1 Money Couple; Shannon McNay: Writer for Student Loan Hero; Rod Griffin: Director of Public Education at Experian and Mike Delgado: Director of Social Media at Experian.

Nikki Vos

The range of topics that couples should consider when planning their retirement is huge, indeed staggering in scope. It’s not a surprise that families focus on what seems simple to calculate, that is, on how much to spend, and how much money needs to be saved. Even those questions are not simple. They are the tip of a big iceberg; the question of how you want to live in the years when you don’t have to work.

We see many couples who came to understandings about each other many years ago, and who have been running on autopilot since then. Major life events such as having children, children leaving the home, or medical problems can cause spouses to re-examine their assumptions and reset their understandings. Retirement as a life change needs to be considered the same way, but we see relatively few couples who have that view. Perhaps they are too excited to leave work to think about the big changes that may be looming!

As financial planners, we get to see folks who know they need more information to get ready to retire. We encourage them to analyze their financial needs after they talk with each other about the fundamentals: do you both want to live the same way when you don’t have to work? When John and Mary want to travel, does he mean an RV for six months of the year while she is heading to Italy for a three week guided jaunt? How much do they want to pass on to the kids, and how will it look?

Our observation is that each spouse has a very different idea about financial security and that it is rare for them to recognize those differences in each other.

Disclosure: Securities and advisory services offered through National Planning Corporation (NPC), Member FINRA/SIPC, and a Registered Investment Adviser. Please consult with your representative to find out on which company’s behalf services are being provided. Varra Financial Associates, Association for Long-term Care Planning (ALTCP) and NPC are separate and unrelated companies. The opinions voiced are for general information only. They are not intended to provide specific advice or recommendations for any individual and do not constitute an endorsement by NPC. To determine which investments may be appropriate for you, consult with your financial professional.

Steve Chen

https://www.newretirement.com/

Here is one of the eight topics that can help you survive retirement with your spouse:

No one wants to think about — let alone discuss — the possibility of a long term care event.

However, the reality is that one of you is likely to experience an event like a stroke, diabetes and plain old age that will require you to need help with your care. Forty-two percent of people over the age of 65 require, or will require, long term care and neither Medicare nor Medicare supplemental insurance cover the costs of these services – neither in your own home nor in a nursing facility.

Without a clear plan in place, the burden of your care will fall on your spouse. Though many individuals consider it an honor to tend to their loved one, you might want to clarify each of your thoughts on this subject and budget appropriately — can you afford assisted living? in home assistance? Furthermore, what happens to the remaining spouse after one of you has passed. What is the plan for the surviving partner?

Download the Top 10 Reasons to Get Long Term Care Insurance to learn how you can secure the future through comprehensive coverage now.

Chelsea Brennan

https://www.mamafishsaves.com/

Here are some questions from Mama Fish Saves that can help you get started with money conversations with your spouse and handle debts as a couple:

- How much debt do you have outstanding? What is your credit score?

- Should each spouse pay down their pre-marriage debt separately, or are you taking the “all-for-one and one-for-all” approach?

- Are you only making minimum payments or paying down principle? When is each debt expected to be paid off?

- How do you feel about carrying a mortgage? Do you want to pay it off over the standard 30 year period or pay it down early?

Do you believe in using credit cards? Do you pay off the entire balance each month or have outstanding credit card debts?

Money Smart Guides

https://www.moneysmartguides.com/

We lifted one tip from Money Smart Guides’ article about money mistakes couples make that destroy their relationship and it’s about responding to needy family members.

This can be a real issue in a relationship. How will you deal with a family member who comes to you for financial help? Hopefully, you will never have to deal with this, but it is smart to talk about it ahead of time as it can be extremely stressful.

Talk about who you would help out and who you wouldn’t and the situations for helping or not. Also talk about what the help would look like and what limits or restrictions you would place on the loaning of money.

The reason why you want to talk about this one now is because you are not emotionally involved. It is much easier to come to an agreement now than it will be when your spouse’s brother is standing in your living room.

![]()

Kerry Hannon

Here’s an excerpt from Kerry Hannon’s “Couples and Money Advice After 25 Years of Marriage.”

Maintain individual and joint accounts

We hold joint savings, checking and investment accounts. But we also have separate retirement accounts (which we’re diligent about funding) as well as separate bank and credit card accounts. This is vital, especially for women. Having your own accounts allows you to establish a good credit record of your own. I call this financial independence.

Peg Webb

https://www.wealthenhancement.com/

For many couples, discussing personal finances is uncomfortable—but it’s a necessary part of seeking financial success. Bruce and Peg have your list of the five key questions you need to ask.

Questions discussed include:

What is the most common mistake you see people making in their investment portfolios?

I’m looking for a financial advisor to help me transition to retirement. What questions should I be asking?

At what age should someone switch from investing in the stock market to more conservative and invest in fixed income-based options?

You can listen to the podcast here:

Start Money Conversations Early

Discussing money, expenses, savings and other factors required in retirement planning with your spouse can be daunting and uncomfortable. But, this is the only way to achieve financial independence in the future. Not to mention that money conversations also give you peace of mind, that everything is set into place, your assets, health and family’s security are safe from major financial meltdown.

Be in control of your future and your family’s future by talking about money and finances as early as possible.

One thought on “11 Experts Share Money Conversations Couples Should Have Before Retirement”