Almost everyone is guilty of committing retirement planning mistakes that would hurt their chances of achieving financial security in retirement. There are myriad of reasons behind these common mistakes that retirees are guilty of doing.

One is the unfamiliarity of people when it comes to planning for retirement. Another is stick to a strategy that worked in the early years but detrimental in the long run. Or, your financial advisor misguided you.

It’s best to be familiar with these mistakes to avoid incurring costly missteps that might derail your retirement.

Top Nine Retirement Planning Mistakes

Mistake #1: Waiting to Plan for Retirement

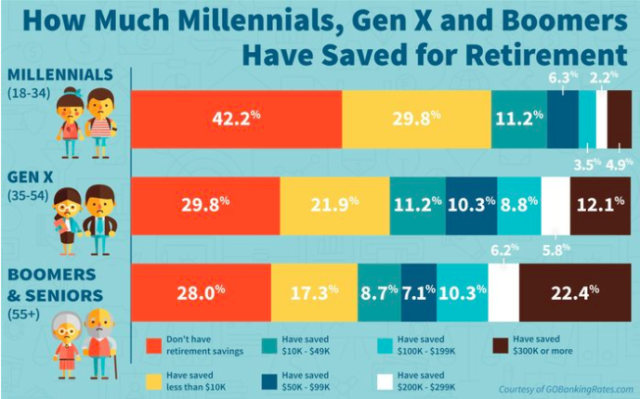

GoBankingRates conducted a survey aimed at Millennials (ages 18 to 34), Gen Xers (ages 35 to 54) and Baby boomers and seniors (ages 55 and over) to find out how the saving patterns of one generation differ from another. Here’s a chart showing that Millennials are least likely to have retirement savings.

Age shouldn’t be a deterrent when saving for retirement. In fact, Cameron Huddleston, Life + Money columnist for GoBankingRates said this:

“The earlier you start saving, the easier it is. Thanks to the power of compounding, if you start regularly setting aside even small amounts as soon as you start working, you could easily have enough for a comfortable retirement.”

There’s no best age to begin planning for retirement and saving money. Stop putting it on hold and start planning for your financial future. Facing financial woes in the future is worse than starting a retirement plan today.

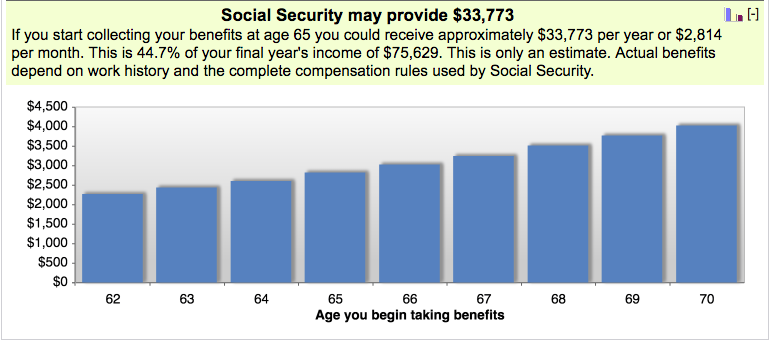

Mistake #2: Applying for Social Security Benefits Too Early

Applying for Social Security Benefits can be done once you turn 62. However, the benefits you’ll receive will be around 35% less than what you would receive if you wait until your full retirement age.

It’s not advisable to get your Social Security benefits before your full retirement age unless you really need money. If you can afford to put off applying until age 70, you will receive benefits 32% higher than what you would receive on your full retirement age.

Here’s a sample estimate of the benefits you can receive from Social security

For a more accurate estimate, you can use Social Security’s calculator that will give you an idea of your benefit based on your date of birth and earnings history.

Mistake #3: Making Bad Assumptions

Your retirement plan consists of projections that would show whether you would reach your goals in the future or not. Having unrealistic expectations is not healthy because you might face a different future than what your projections are telling you.

It’s recommended to consider all factors that could alter your retirement and have conservative expectations. Consider factors like inflation and retirement expenses that might put a dent on your savings or worse, will wipe out your nest egg.

Also, consider longevity. People are living much longer today due to the improvements in medicine and technology, which can affect the outcome of your retirement.

Read: 5 Major Retirement Expenses You Should Plan For

Mistake #4: Spending Too Much in Retirement

Nothing is more fulfilling than spending your hard earned money on things you’ve been dreaming of while you were still working. However, you need to consider that you no longer have a steady paycheck or you’re retirement income might not be as high as it was before.

But don’t compromise your retirement lifestyle you’ve always dreamed of. Create a conservative budget that allows you to enjoy retirement and at the same time will still give you enough funds for 20 or 30 years more.

It’s a good idea to speak to a financial advisor who can help develop a strategy for your preferred retirement lifestyle for as long as you’re alive.

Mistake #5: Underestimating Long Term Care Costs

According to recent research by U.S Department of Health & Human Services, around 53% of Americans turning 65 today will develop a disability that would require long term care services and supports (LTSS).

The cost of long term care facilities and services today are rising. On average, an American will have to pay $97,455 annually for a private room in a nursing home and $85,775 annually for a semi-private room in a nursing home. Below you can find the current average cost of care.

We created an interactive map that will show you the average cost of care by state, and give an idea of the current state of long term care costs today.

It’s imperative to include long term care in your retirement plan, to protect your savings and also your loved ones from the devastating cost of long term care. It’s best to buy long term care insurance, an insurance policy tailored to fit a policyholder’s care needs and helps pay for long term care expenses.

It is recommended to request for free quotes first and compare long term care insurance policies from different companies to find the best available policy perfect for your needs.

Download our free e-book Long Term Care Insurance and Retirement: 8 Essential Questions to learn more about how the policy works.

Mistake #6: Overlooking Estate Planning

One of the most overlooked factors when planning for retirement is estate planning. Some Americans forget to take the necessary steps to protect their financial assets when they are no longer here.

Without a proper plan in place, your children will have a hard time managing everything you left for them. While there is still time, create an estate plan and prepare these legal documents:

- Living trust – a document that puts your assets into a trust during your lifetime. When you pass away, your assets will be passed to your beneficiaries.

- Durable power of attorney – allows the person you’ve chosen to manage your estate when you can no longer make decisions.

Make sure to inform your loved ones about your wishes and these documents.

Mistake #7: Failing to Make a Conservative Investment Approach

When you were still younger and working, you can max your contributions because you can still earn money and make up for your losses. But the game changes as you approach retirement. You need to make adjustments to your investments since you will need to use the money you saved for your daily expenses.

It’s recommended to preserve your assets especially during the beginning of your retirement. If you’re not cautious, your actions will have a negative on your retirement portfolio and you might have a hard time to recover.

Mistake #8: Not Talking With Your Spouse

Couples planning for retirement often forget to talk about the effect of the transition from working to staying at home and enjoying retirement. They should talk about different money conversations that couples should have before retirement.

It’s important for married couples to be on the same page and to have the same plans for their future. They should practice the art of compromising to maintain a harmonious relationship and also to create a sound retirement plan that will secure their future.

Mistake #9: Overlooking Maxing Out Your Retirement Contributions

It’s recommended to max your 401(k) contributions if your employer offers it. By saving pre-tax via the 401(k), your employer offers will give you more savings when you save after tax.

Auto-enrollment is very convenient but better keep an eye on this because there are instances wherein employees are auto-enrolled but at saving rates lower than the amount they would have chosen.

You can contribute additional savings through catch-up contribution if you’re 50 years old or older.

Oooh this is super useful, especially with your graphs you have on here. I’m a Millennial and I’m happy to say that I am ahead of some of the peers that I know. I could do better and I am working on it.