It’s never too early to plan for retirement given the circumstances today – longevity and expensive health care and long-term care costs. Despite this stark reality, there are still some Millennials who put saving for retirement at the bottom of their priority list.

Millennials’ retirement looks bleak right now because of their inability to handle their competing priorities – college loans, debts, rent and monthly bills, looming long-term care needs and to save enough money for retirement. Putting off saving money for retirement causes a ripple effect that can delay their retirement or worse, leave them with nothing for retirement.

A new report by the National Institute on Retirement Security reveals the troubling outlook of Millennial on retirement. According to the report, 66% of working Millennials have nothing saved for retirement.

But not all Millennials are behind on saving money. In fact, one-third of 83 million Millennials are saving for retirement. Their average account balance in the bank amounts to $67,891.

But will their saving habits and attitude towards retirement enough to give them a bright future?

To answer this question, we’ve curated five articles that reveal shocking facts about Millennials’ retirement and different ways to overcome their retirement planning challenges.

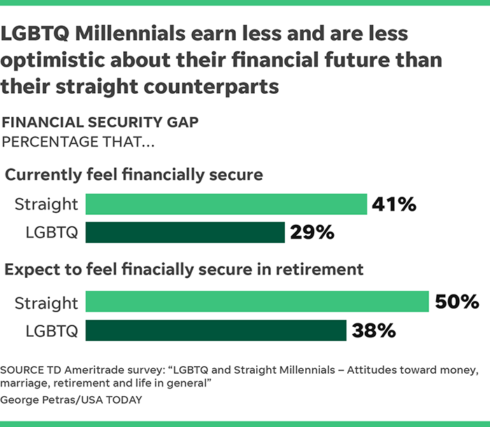

American Dream Tough to Achieve by 40 Says LGBTQ Millennials

A financial study about LGBTQ Millennials published in USA Today analyzes the differences on how LGBTQ (lesbian, gay, bisexual, transgender, questioning) and straight Millennials view their retirement – living the American dream. Although there are some similarities in the saving habits of LGBTQ Millennials and their counterparts like they save the same percentage of monthly incomes, pursue traditional career paths, and they will most likely invest in stocks there are also significant discrepancies.

The key differences reveal that LGBTQ Millennials are behind in financial literacy, salary, and confidence in retirement. Their lack of confidence is what holds them back, which hinders them to improve their financial situation when they retire.

However, these financial disparities can be reversed by increasing financial literacy, making the most of your company’s 401(k) and knowing your value at work. LGBTQ Millennials are still in the game as long as they are proactive in planning for retirement.

Unique Financial Planning Challenges Millennials Should Overcome

The uncertain future of Medicare and Social Security, longevity and saving money are some of the major retirement challenges that Millennials are facing right now. Main Line Today’s article discusses the most important issue younger investors are facing right now – healthcare. The uncertainty of the cost of healthcare and availability of healthcare options 30, 40 and 50 years from now is scary.

Since nobody knows what would happen in the future, whether Medicare will still be there in case people will need care, it’s best to prepare for this kind of life events by setting up health savings accounts. According to Chuck Creighton, a financial advisor of Media-based Evolution Financial Group, highly recommends maximizing contributions to health savings plans to have enough disposable income that they can use for their future healthcare needs.

Before, people don’t consider longevity. But now, longevity is an integral part of Millenials retirement plan.

Read: Securing a Fail-safe Retirement Plan: Steps to Take by Age

Cryptocurrencies as a Money-Saving Tool

According to Bitcoinist.com’s Millennials are Buying Cryptocurrencies to Save For Retirement, cryptocurrency is an investment trend is becoming popular among Millennials today.

Instead of doing traditional ways to save money for retirement, Millennials are embracing modern retirement solutions created by innovative startups. Investing in Bitcoin works well if you have different types of short-term and long-term assets in your portfolio and you have IRA or other tax-advantaged plans.

Today, you can already put Ethereum, Bitcoin and other types of cryptocurrencies in an IRA. These are worth a try given that there are only a handful of alternatives and besides Millennials are known to be tech-savvy.

Millennials: The Future of American Caregiving

According to a new report by AARP, a quarter of family caregivers today are millennials, which are nearly 10 million of the United State’s 40 million caregivers.

Taking care of an aging loved one is fulfilling, but it also poses unique challenges that make it hard for caregivers to do their task and at the same time attend to their other responsibilities like going to work. Millennial caregivers spend around 21 hours per week taking care of their loved ones, which is equivalent to having a part-time job.

Amidst these struggles by Millennial caregivers, AARP is striving to raise awareness on the issues experienced by younger caregivers that can open doors to a more supportive environment. Also, to give Millennial caregivers a chance to work, build income and prepare for their future.

Read: Family Caregivers: The Everyday Superheroes

Surprising Millennial Money Facts

Millennial money mix-ups are prevalent today because of student loans, low financial literacy, and other financial challenges. To help you avoid these financial sins, RuntheMoney.com shared 5 Millennial Money Facts that Will Make You Say OMG.

One of the things that you can learn is refinancing your student loan debt, which is not just a burden today but also already a national crisis. Refinancing can ease the burden of paying for student loans and can help Millennials save more money for retirement. Unfortunately, only 34% or one-third of college-educated Americans are aware of this and have refinanced their student loans.

Millennials should take advantage of refinancing their student loans so that they can pay their debts in a shorter period and they can live a retirement they’ve always dreamed of.

Final Thoughts on Millennials’ Retirement

Millennials still have a long way to go before retiring. But, it’s not an excuse to delay managing their finances. So as early as now, Millennials should start addressing their financial issues and preparing for retirement. Paying debts is a good start, improving their financial literacy can pay off in the future, being open to new investment opportunities and preparing for future caregiving tasks can help Millennials save enough money and enjoy retirement.