Have you considered health care costs as one of the major retirement expenses you should plan for now?

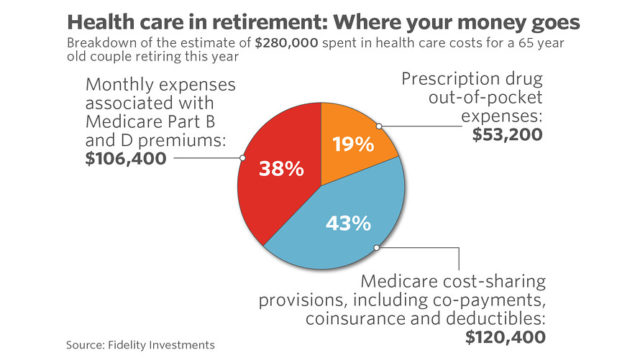

If not, then make sure you’re ready to shell out a considerable chunk of money to cover healthcare and medical expenses. According to Fidelity Investment’s annual retiree health care cost estimate, a 65-year old couple retiring this year would need $280,000 to pay for their health care expenses. As for individuals who would retire this year, a man would need $133,000, and a woman would need $147,000. It would cost more for women because women are expected to outlive men.

Here’s a breakdown of where the $280,000 would go.

But what’s alarming is the fact that these numbers don’t include long term care cost, which is very expensive. Here is the current average cost of long term care today.

Thankfully, there are myriad of ways you can manage long term care and health care costs in retirement. Also, there are several states that offer affordable long-term care facilities.

Check out this map infographic of top 10 U.S states that offer cheap long-term care.

Ways to Save on Health Care Costs in Retirement

1. Stay as Healthy as You Can

One of the most effective ways to control the rising cost of care in retirement is by staying as healthy as you can. Here are some tips that can help you stay healthy.

- Include exercise in your everyday life.

- Avoid processed foods as much as you can.

- Get rid of your bad habits.

- Visit your doctor regularly.

- Stay hydrated.

- Reduce stress.

- Express yourself.

- Be consistent and do everything in moderation.

2. Address Health Issues Early

Being nonchalant to minor health issues is risky since it can quickly escalate to becoming an issue that is detrimental to your health. You can save a lot of money on the cost of health care when you retire if you address your health issues before they get worse.

A simple cold or a cough might turn into something more severe if you opt not to take over-the-counter medications or see a doctor. Chances are, you’ll get hospitalized, and you’ll be slapped with a hefty medical bill. So, get to the root of the problem right away to avoid paying for expensive health care costs.

3. Buy Long Term Care Insurance

Around 7 out of 10 Americans 65 years old and above will require some form of long term care, according to the U.S Department of Health and Human Services. In addition to that, the cost of long term care continues to rise every year.

Staying in a private room in a nursing home will cost you $97,455 annually. An assisted living facility, on the other hand, will cost you $45,000 annually.

How do you plan to pay for it?

Buying long term care insurance can help you save on long term care costs, protect your nest egg, help you avoid becoming a financial burden to your loved ones and it can also give you peace of mind.

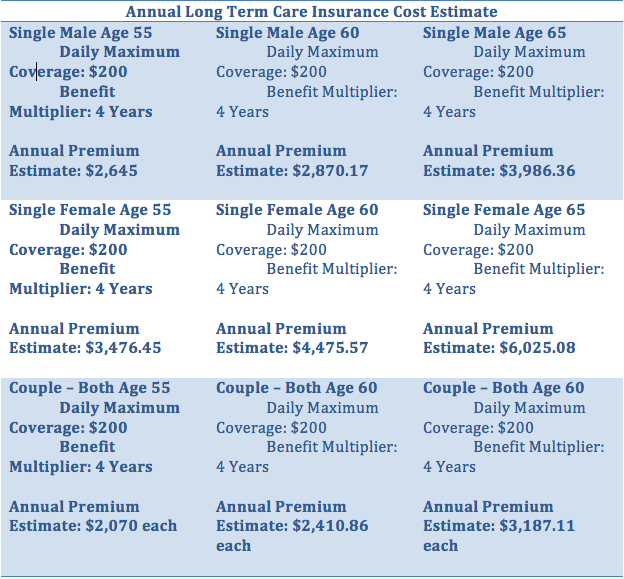

If you want to save on premiums, you should buy insurance for long term care while you’re in your 50s or 60s. Make sure to request instant quotes for long-term care insurance to find the best available policy perfect for your potential care needs. Here’s a table of the estimated cost of long term care insurance.

Read: Should I Get Long Term Care Insurance [Infographic]

4. Avail Medicare Supplement Insurance

You become eligible for Medicare benefits when you turn 65, which include annual wellness visit to your doctor, critical health screenings such as cancer screenings, depression screenings, diabetes testing, and mammograms.

However, some medical tests and procedures that are not covered by Medicare. This is when Medicare supplement insurance comes into the picture. It’s a private health insurance that pays up to 20% of expenses that Medicare does not cover. Availing this type of policy can help you save a significant amount of healthcare expenses.

5. Options for Early Retirement

In case you retire before you become eligible for Medicare and your company doesn’t cover medical coverage for retirees, here are some of the options you can explore:

- Enroll in Medicaid if you’re eligible.

- If you’re married and your spouse is still working, you can add yourself to their coverage.

- Find coverage through your local health insurance broker.

- Continue your coverage through COBRA until you find a better solution but this is a costly option.

- If you decide to work part-time, ask if your employer offers medical coverage and if you’re eligible.

Read: 9 Retirement Planning Mistakes You’re Guilty of Doing (New Data)

6. Consider an HSA

Explore the possibility of funding an HSA or Health Savings Accounts. Your funds can be used to pay for medical expenses now or in the future. If ever you will not use your pool of money yet, then this will be allowed to accumulate and you can use your HSA funds to pay for health care insurance or medical expenses in retirement.

One thought on “6 Useful Tips to Avoid Paying $280,000 Health Care Costs in Retirement”