Contrary to the popular belief, Medicare doesn’t pay for long term care, such as nursing home, home healthcare and other forms of long term care. In case you’ll need long term care in the future, you might end up outliving your retirement savings.

Long term care insurance is designed to help individuals pay for long term care services and facilities in the event that they can no longer carry out at least two of their Activities of Daily Living (ADLs) – eating, bathing, dressing, toileting, transferring and incontinence.

But what does long term care insurance cover?

Here’s everything you need to know.

Long Term Care Facilities and Services

A long term care policy pays for different types of long term care facilities and services in different locations. Take note that that price differs depending on the state you live in. Long term care in some states can be very expensive while there are some states known for affordable long term care.

This policy gives you the liberty to choose the perfect facility or service that is right for your needs. You can receive care and use long term care insurance in any of the following:

Home Care

Many Americans think that this type of policy only pays for nursing homes. In fact, one of the benefits of having long term care insurance is the ability to age in place.

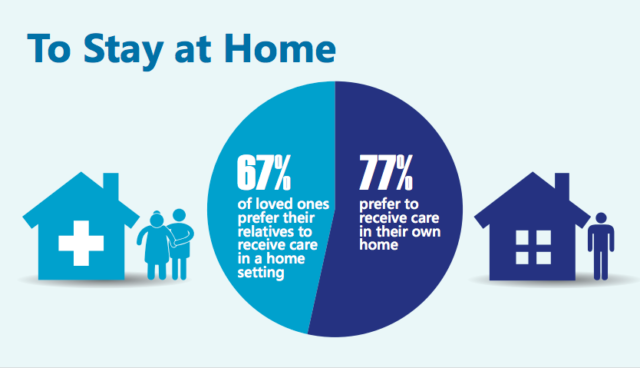

Based on an ALTCP Infographic, 77% of Americans prefer to receive care at home.

The number of aging Americans who want to stay at home and will need any form of assistance is rapidly growing. Unfortunately, traditional government health care programs can’t keep up with this growth. So, aging Americans look for other payment options such as long term care insurance that will help them fund their care needs at home such as companionship, assistance in ADLs, transitional care, medication management and more.

Related: 15 Tips for Independent Senior Living That Actually Work

Nursing Home

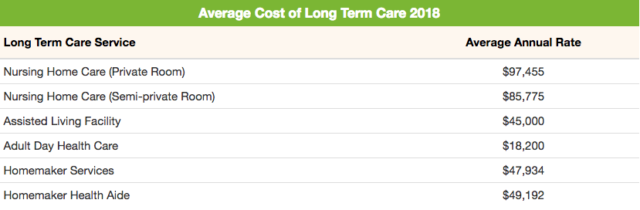

The average annual cost of a private room in a nursing home today is $100,379 while the average annual cost of a semi-private room in a nursing home is $88,348. It costs a lot today and it will cost more in a few years.

Aside from the cost, you should also consider the length of time you’ll stay in a nursing home. The average length of stay in a nursing home facility is 183 days or more than two years. But those with cognitive condition will have to stay in a nursing home for about 5 years.

Having insurance for long term care insurance will be very handy when the time comes that you need to move in this kind of facility considering its rising cost. As a matter of fact, around 5% of the total U.S nursing bill is paid by long term care insurance.

Read: 6 Ways You Can Protect Your Assets From Expensive Nursing Home Costs

Assisted Living Facilities

You may require more assistance as you age but it doesn’t have to be losing your independence. You can opt to live in assisted living facilities where you can retain some of your independence while receiving care.

Long term care insurance pays for assisted living. But since policy features and benefits vary depending on your insurer and your type of policy, its best to determine your needs first, specify the coverage and find out how you can qualify for benefits to avoid delays or decline in payment later on.

There are some unfortunate cases wherein policyholders were denied of coverage for assisted living because they bought their policies in the late 80s and early 90s, the time when assisted living facilities aren’t a thing yet and before policies offer more comprehensive coverage.

To avoid being denied coverage or getting some coverage only, here are some policy dilemmas highlighted by the California Health Advocates in their report.

- Some long term care insurance companies refused to pay for assisted living care because it doesn’t meet their requirements for staffing, services or design. Some stipulations include that an assisted living facility should have a minimum number of beds or that nursing care must be present for 24 hours.

Make sure that your long term care insurance policy provides coverage for an assisted living facility to avoid problems in the future. Also, it pays to be aware of the stipulation and eligibility requirements so that you can make the most of your policy.

Read Next: 7 Efficient Ways to Pay for Assisted Living Facility

Adult Day Care

Adult day care is a type of long term care that family caregivers would find helpful especially those who have jobs and those who want to take a break from caregiving. This type of care is typically a sitting service wherein the care recipient receives supervision and limited care while family caregivers do other responsibilities.

The median cost of adult day care is $72 a day, $1,563 per month or $18,746 annually. It’s not that expensive compared to other types of long term care but it’s still wise to consider getting a long term care coverage considering that the cost of care continues to rise. Also, instead of paying out-of-the-pocket, which you can spend on other expense, you can use long term care coverage instead.

Alzheimer’s and Dementia Care Costs

One of the most important things you need is to consider all the costs you might face later in life due to a cognitive condition such as Dementia and Alzheimer’s. Take note that these are progressive conditions, which means the level of care you’ll need will change over time.

It’s best to estimate the cost of long term care facilities:

The cost of Alzheimer’s and Dementia care can become more expensive if you opt for senior living communities that specialize in memory care. It may be a lot expensive but it’s an all-inclusive package and you’ll be assured that you’ll receive proper care since the facilities specialize in treating patients with a cognitive condition.

On top of the cost of facilities, you need to anticipate the cost of prescription medication, which costs around $150-$200 per month.

It’s wise to buy long term care insurance if you have a family history of cognitive condition because you can no longer apply for coverage if you’re diagnosed with Alzheimer’s.

Relying on your family members should not be an option. Taking care of an individual with Alzheimer’s or Dementia has an average out-of-pocket cost of care amounting to $61,500 according to Annals of Internal Medicine.

In case you already have long term care insurance, make sure to review your policy to double check if it covers Alzheimer’s or Dementia care and find answers to these questions:

- Does your policy pay for Alzheimer’s?

- What is your daily benefit? Do you have inflation protection?

- How long will you receive benefits?

- Is there a maximum lifetime payout?

- What type of long term care settings and services your policy cover?

- How long will your policy start to pay after your diagnosis?

- Do you have tax obligations for receiving benefits from your policy?

Read Next: 6 Quick Ways to Manage the HIght Cost of Alzheimer’s Care

Additional Long Term Care Insurance Benefits and Features

Home Modifications

As I’ve said earlier, many aging Americans prefer to stay at home than to move to a nursing home or any type of facility. According to the Home Care Association of America, the average age of the majority of home care recipients is 69 years old. 3 out of 5 or 59% of care recipients have long-term physical conditions and 26% have a cognitive condition.

Home care is appealing to the aging population because it’s comfortable, familiar, affordable compared to other long term care services and setting and promotes peace of mind for families. But in order to make sure that you’ll age safely and securely, you need to consider home modifications that will prevent falls, accidents, and injuries.

You can use your insurance for long term care to install these home modifications:

- Electric outlets and accessible light switches

- Grab bars

- Low-pile carpeting or other types of flooring

- Power recliner or chair

- Raised toilet

- Stair lift

- Stair or bed rails

- Walk-in shower

- Wheelchair ramp

- Wider doorways

Coordinated Care

You can assign a care coordinator that helps assess your needs and create a plan of care if you have long term care insurance. This will come handy if you need additional guidance in planning for long term care. It also helps in coordinating care when on a claim.

Cash Benefits

Many Americans today take care of their loved ones. In fact, 43.5 million provide unpaid care in the United States. But if you have long term care insurance with cash benefit feature, you can use your benefit in any way you want. This policy feature is perfect for family caregivers who provide care to their aging family members.

Before buying coverage, look for a policy that pays cash benefit when care is given my family and friends.

Personal Assistance With Daily Care and Therapies

Long term care insurance coverage also pays for the following services:

- Hospice Care

- Housekeeping & Errands

- Occupational Therapy

- Physical Therapy

- Post-hospitalization Care

- Rehabilitation Therapy

- Respite Care

The Bottom Line

Long term care is a reality that Americans should acknowledge and start planning for early. Getting long term care insurance is the best option you have right now since it provides comprehensive coverage, which can give you peace of mind since you know that everything you might need in the future will be covered.