While most of us avoid talking about our demise and looking into effective estate planning tips, it’s impossible to dodge discussing end-of-life-financial from family members. Nobody knows when our time is up, so it’s best to prepare an estate plan before the inevitable happens.

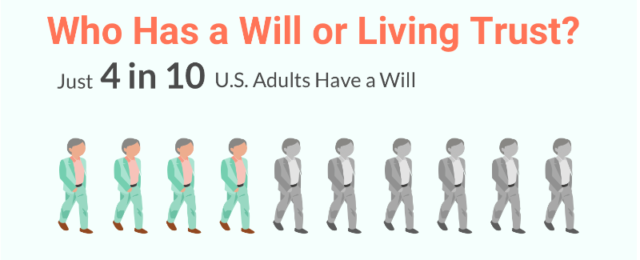

However, the importance of having an estate plan isn’t reflected in the behavior of Americans on the survey data collected by Princeton Survey Research Associates International. According to the survey, 6 out of 10 of Americans don’t have an estate plan, which means they might lose all their assets, cost their families thousands of dollars and dispute among family members might arise.

In line with the National Elder Law Month, ALTCP came up with effective estate planning tips that can ensure to distribute their assets based on their wish.

Must-Do Estate Planning Tips

- Plan for long term care

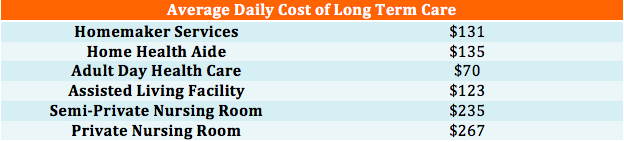

High long term care costs could eat up your entire nest egg and leave your family with nothing or worse, in deep financial obligation due to devastating long term care expenses.

The cost of long term care differs from one state to another, but they have one thing in common, it continues to rise. Here’s a table of the average daily costs of long term care across the United States.

To prevent long term care expenses from eating up your assets, you should develop a long term care plan to fund their care expenses through a long term care insurance policy.

Fill up this 6-second form to get free quotes for long-term care insurance from leading companies.

- Make a physical and non-physical items inventory

Make a list of valuable things that you can find inside and outside of your homes like laptops, appliances, jewelry, collectibles, vehicles and other items that are worth a hundred dollars or more.

Also, create a list of non-physical assets such as digital financial assets including cryptocurrencies like Bitcoin, Litecoin and Ethereum Ripple. You should list down insurance policies as well as long term care insurance, health insurance, life insurance, car insurance and more. Include your other assets too like savings accounts, 401k plans, IRA assets, brokerage accounts and others.

- Create Living Wills or Advance Health Care Directives

These documents contain instructions on how you want to be taken care of when the time comes that you can no longer decide for yourself. Through living wills or advance directives, you can create written instructions on how you want medical assistance or custodial care to be administered when you can no longer decide for yourself.

- Create Medical Power of Attorney

A medical power of attorney allows you to designate a person who will make important decisions regarding your health if you can no longer make or communicate wishes about your health care.

- Create a Living Trust

Creating a living trust gives you the power to place your assets into a trust that you can use during your lifetime. If you pass away, your assets will be passed on to your chosen beneficiaries. Trusts are advisable for people with complex or substantial financial estates.

- Create a Durable Power of Attorney

A durable power of attorney allows you to choose a person who will manage your estates. Make sure to inform your family and friends about your wishes and other essential details. It’s important that the person you will choose is comfortable with this type of responsibility.

- Test your power of attorney

The only time you’ll know if your power of attorney is good is when you use it, and that’s when you’re already incapacitated and too late to create a new one. Test your power of attorney while it’s still early to make sure that financial institutions would accept it. Keep in mind that each financial institution will perform a different test to a power of attorney to determine its validity.

- Review and update estate plan regularly

Review your estate planning documents regularly. Do it once in two years or after major life-changing events like death, birth of child, marriage, and divorce. It is recommended to review your estate plan to make sure that it still reflects your wishes and remains relevant.

- Review savings and retirement accounts

Beneficiaries you list in savings and retirement accounts pass via a contract to that certain person listed at your death. The beneficiary listing will take precedence, so it doesn’t matter how you list these accounts in your trust or will. Make sure to review your savings and retirement accounts to make sure that the beneficiaries are listed exactly as you wish.

- Keep Legal Documents Safe and Accessible

Having these estate planning documents are useless unless your heirs know where to find them. Don’t keep these documents in a safe deposit box in a bank because your heirs may not be able to access the deposit box unless a court order is issued.

- Consider College Funding Accounts

Take advantage of college funding accounts such as the 529 plans, which provides tax advantages while paying for higher education. However, most universities don’t accept 529 plans if a grandparent is listed as the custodian. The best thing about 529 plan is that the growth and withdrawals are tax-free if it is used for qualified education expense.

- Make annual tax-free gifts

Take advantage of making annual tax-free gifts. You are allowed to make a gift of up to $15,000 without triggering taxes.

- Ask Help from Financial Planner or an Estate Attorney

It’s always a good idea to seek the help of a professional. In this case, a financial planner or an estate attorney. Doing a little research on estate planning tips first can help get your estate plan in check and can also help minimize the cost of professional help.