People buying long-term care insurance are focused on just one issue and that’s whether it’s worth the price. According to a study by the U.S Department of Health and Human Services, approximately 70% of individuals 65 and above will require long-term care supports and services during their lifetime.

Obviously, there’s a need for this policy. But if you buy based on the price only, then you might find yourself in deeper financial trouble later on.

Why?

You might end up buying a policy that doesn’t cover your long-term care needs. There are other issues that individuals should look into including small details that don’t seem to matter now but will have a big impact once you’ve decided to buy long-term care coverage or when you start receiving care.

To help you make a well-informed decision, here are some costly mistakes that you need to avoid when shopping for long-term care insurance.

Waiting too long to get coverage

People have different reasons why they delay buying a policy. Some think that they will not need it while others are confident that they can rely on health insurance, Medicare or Medicaid to pay for their long-term care expenses. These stem from misinformation that will cost consumers a lot in the future.

Here’s the truth: Health insurance and Medicare doesn’t pay for long-term care, but Medicaid gives coverage to people who can’t pay for care.

According to experts, the best time to buy a policy is when you are in your 50s. This is when retirement is just a few years away, the perfect time to eliminate debt, save more money and buy insurance for long-term care. Most importantly, this is when premiums are more affordable and it’s the easiest to qualify for coverage.

If you wait for a few more years before you get coverage, you might end up paying more for your coverage since insurers increase premiums simply because an applicant is a few years older.

You might also end up not qualifying for coverage if you wait too long because of health issues.

Buying a policy you won’t be able to afford in the future

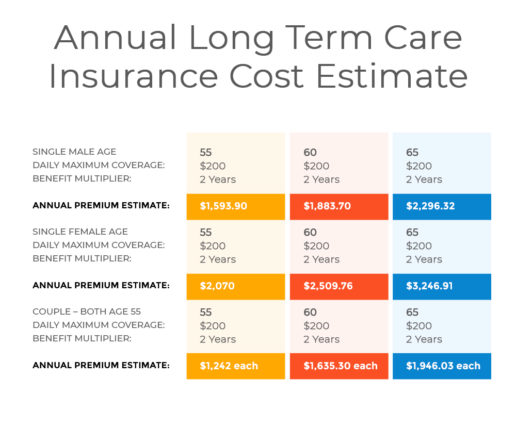

The estimate cost of long-term care policy for a 55-year old male with daily maximum coverage of $200 and benefit period of 2 years is $1,593.90. But the real challenge comes during retirement. Policyholders might encounter premium hikes that would make it difficult for them to fit high premiums in their retirement budget and many end up dropping policies they can no longer afford.

To avoid this scenario, individuals can seek the help of a financial planner that can help them fit their premiums into your projected budget during retirement before buying insurance.

Underestimating impact of inflation

If you buy a policy in your 50s and won’t use it until your 70s or 80s, years of inflation will eat up a big chunk of your benefit. There’s a reason why insurers offer inflation protection. Unfortunately, many individuals overlook this policy feature.

Adding inflation protection to your policy will cost you 40% to 60% more. This is probably the reason why many individuals skimp on their policies and forgo inflation protection. But if you take a look at it closely, adding simple inflation, compound inflation or guarantee purchase option protection is the better option considering the rising cost of long-term care today.

Overlooking shared care benefits

Did you know that couples could share policy benefits instead of buying two expensive policies?

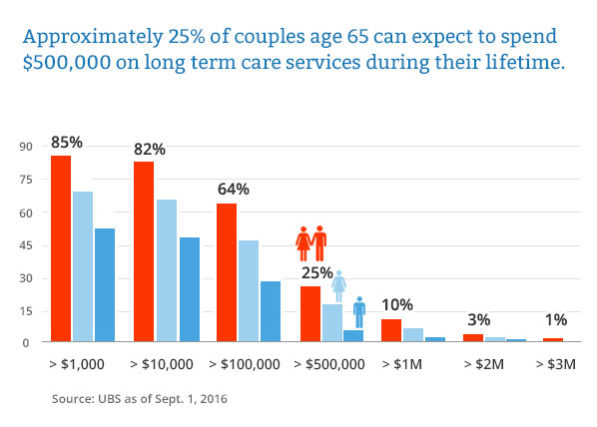

Through the shared care rider, couples – married or not – can double their benefits without overspending. This is perfect for couples since the cost of care continues to rise and based on studies, around 25% of couples 65 years old and above can expect to pay for half a million on their long-term care needs.

If both individuals have three years worth of coverage, they can combine their benefits into a pool, and share six years worth of benefits.

Not reading the fine print

Some people who purchased long-term care insurance don’t read the fine print, which results in claim denials that delay the collection of benefits. This can be avoided by understanding the definitions and terms of the contract, so you will know when you can start receiving benefits.

Most policies pay when the policyholder meets one of two of these conditions: must be unable to perform two out of six of activities of daily living – eating, bathing, dressing, toileting, transferring and continence or having a cognitive impairment such as Dementia or Alzheimer’s.

Take note of details such as elimination period, the period of time the policyholder needs to wait before receiving benefits. Also, check if your policy contract mandates that you need to hire a caregiver from home care agencies.

Choosing the wrong insurer

Choosing a long-term care insurance provider that offers the cheapest policy might be the first option for some individuals. But, buying based on price alone shouldn’t be the only factor when buying coverage. Make sure you’re buying from an insurer you can trust.

You might not make a claim for 10 to 20 years or even longer, so it’s important to find a company who is still there to pay your claim when you start to need long-term care. So before buying a policy, compare large and stable companies first including their reviews and financial ratings.

Assuming that group long term care policy is better

Traditional long-term care insurance actually provides better benefits for the same price or at a cheaper price.

How is that possible?

Long-term care coverage purchased outside of an employer setting offers bigger discounts for married or partnered couples and those who are healthy. Couples can get a discount of up to 40% while preferred health discounts are around 10% to 15%.

Group long-term care insurance only covers 50% or 75% of home care, unlike the individual policy that covers 100% of home care.

Related: Group Long Term Care Insurance vs Individual Policy: Which is Better?

Working with the wrong insurance agency

Most insurance agencies have the best intentions for their clients and want the best for them. However, due to limited product access, an insurance agency might not be able to provide the best recommendations.

Find an agency that has access to leading insurers and can help you compare coverage options from the best insurers including Mutual of Omaha, TransAmerica, Genworth, LifeSecure and more.

Ready to Shop for Long-Term Care Insurance?

Shopping for a policy can be a bit overwhelming and that’s why we are here, to simplify your options for you. We will provide you with objective advice, insurance estimate costs, features and benefits of best available policies to help you identify what’s right for your long-term care needs.

To begin comparing your coverage options and to receive your free long-term care insurance quotes, please complete our online quote form or call us at 800-362-8837 today.