Long term care insurance is a wise investment for most Americans today given the scenario that they are getting older – 70% of Americans 65 and up will need long term care and will most likely require expensive long term care. You don’t have to worry about paying for care out-of-the-pocket or becoming a financial burden to your loved ones if you have long term care insurance. Having this type of policy is practical and reasonable. The real issue is, when should you buy long term care insurance?

The logic behind determining the best age to buy insurance for long term care is simple. You can’t buy a policy unless you are healthy and you can’t take advantage of the best rates unless you are healthy too. The younger you are when you buy a policy, the fewer chances you have to develop a condition that will deny your application or increase your premiums.

So, should you buy long term care insurance as early as in your 30’s, in your 50s or when you turn 65?

Should I Buy Long Term Care Insurance In My 30s?

You should be learning how to be more responsible in handling your money when you reach your 30s. This can mean a lot of things and one of them is buying insurance products such as long term care insurance.

Is long term care insurance worth buying that early?

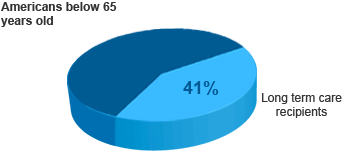

Without it, an illness, accident or injury can leave holes in your pocket because of high long term care costs. Contrary to popular belief that only old people will need long term care, approximately 41% of working adults below 65 years old may require long term care.

It’s wise to have coverage as early as in your 30s but keep in mind that purchasing a long term care policy is personal. Everyone’s situations are unique so it’s best to determine your needs first, educate yourself by requesting free quotes from one source and asking the help of a long term care specialist.

Should I Buy Long Term Care Insurance In My 40s?

People in their 40s are considered as either a late baby boomer or a part of Generation X. Regardless of the age group they are included, you should double your efforts in financial planning for your security and your family’s as well.

Including long term care in your financial plan is a must these days. As a matter of fact, the earlier you plan for long term care the better. A long term care insurance policy helps pay for nursing homes, assisted living and other services and facilities that assist individuals who are aging, with chronic illness or disability. But this is a reality that some Americans that don’t entertain until they are old. This means that they are either disqualified for coverage or their premiums are too high.

Your good health has a massive impact on discounts and declines in your long term care coverage. Insurance providers give discounts to applicants who are healthy. Also, the percentage of applicants in their 40s who qualify is high. In fact, around 62% of applicants ages 40-49 are qualified for coverage.

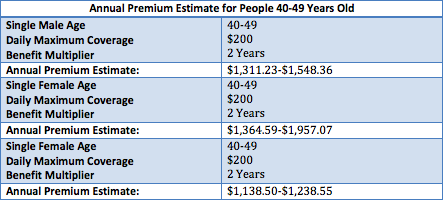

Let’s look at the average cost of long term care for people 40-49 years old.

Should I Buy Long Term Care Insurance In My 50s?

Once you turn 50, you start to realize that retirement is just a few years away. So now is the perfect time to focus on saving more money, eliminating debt and securing your future by buying a policy.

However, many Americans in their 50s are not yet ready for their golden years. According to a survey by Go Banking Rates, 33% of baby boomers or individuals who are 55-64 year olds don’t have savings. But those who have saved $10,000 nearly doubled compared to last year from 17% to 32%. Despite this improvement, these numbers are still alarming considering that this age group has a high risk of needing expensive long term care.

People in their 50s need to take their efforts in saving money a notch higher. But will they have more than enough to retire comfortably?

To avoid outliving your retirement savings and asking financial help from your loved ones, buy long term care insurance that will help pay for the high cost of long term care.

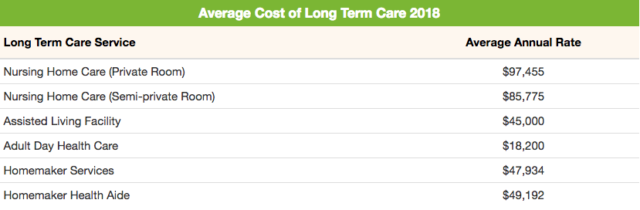

Take a closer look at the current annual median cost of long term care.

Related: Should I Buy Long Term Care Insurance Even If I Can Afford Care?

Should I Buy Long Term Care Insurance In My 60s?

Waiting for too long before you buy long term care insurance has a huge impact on your premiums and your chance of qualifying for a policy. As you grow older, your chance of getting health discounts declines since you are more at risk of developing conditions that might require long term care. It’s not smart to delay buying a long term care insurance policy since you’ll pay more for premiums.

The cost of a policy for a 55-year old is $1,593.30 while the cost of long term care insurance for 65-year-old is $2,296.32.

In case you have a pre-existing condition, your premiums would be higher or worse your long term care policy application will be declined. As a matter of fact, 23% of applicants who are 60-69 years old are declined of coverage.

Your premium is actually just one of your concerns. If something happens and you’re uninsured, you need to pay for long term care out-of-the-pocket, which is expensive.

Read: Give the Gift of Security This Holiday Season: Buy Long Term Care Insurance for Parents

Can I Still Buy Long Term Care Insurance When I’m 70?

You can still buy long term care insurance when you’re 70 but it’s highly unlikely that you’ll get qualified for coverage. This type of insurance has a strict underwriting that you need to pass first in order to qualify. But since you’re old and you might have a health condition, insurers might decline your application. Around 45% of applicants who are 70-79 years old are denied coverage because of health issues.

You can follow these tips to make sure that you qualify for long term care insurance coverage.

So, What’s the Best Age to Buy Long Term Care Insurance?

It pays to purchase a long term care insurance policy as early as in your 50s. You can enjoy health discounts when you get coverage early and you’ll have the peace of mind that you have a coverage that can handle your future long term care expenses.

If you’re ready to compare policies, you can start by requesting for no-obligation quotes from Association for Long Term Care Planning’s designated long term care specialist.