Still looking for the perfect gift for your elderly parents this holiday season? We, at Association for Long Term Care Planning, will help you explore long term care options that can help your parents age the way they want in the future. Fill out our short form to get your free long term care insurance premium estimates.

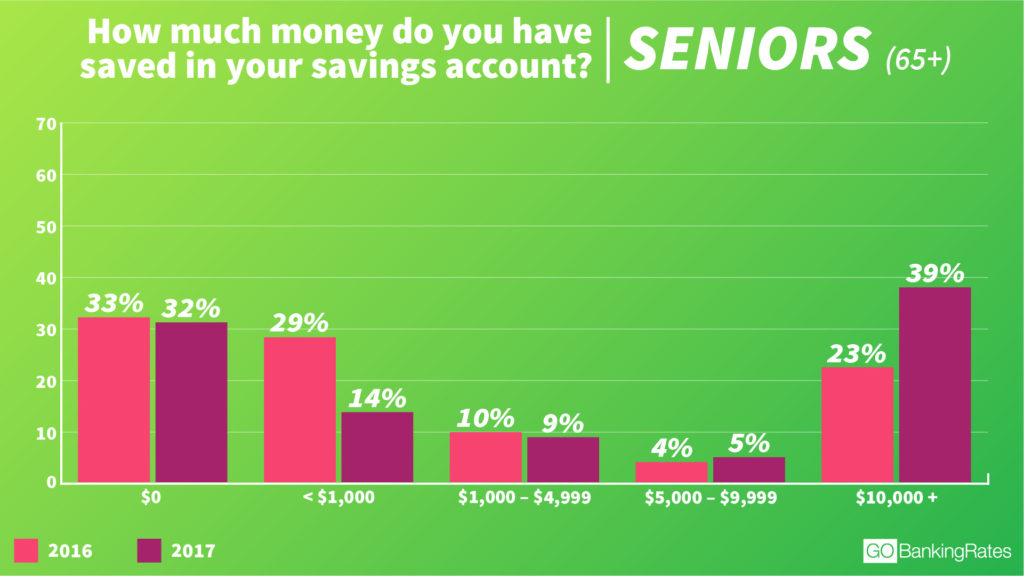

Families avoid talking about long term care as much as they can but it’s a reality that most of them would face sooner or later. Around 70% of individuals 65 years old and above will require long term care due to old age, chronic illness or injuries. If you think your aging parents have saved enough for their future care needs, it is estimated that around 32% of individuals 65 and up haven’t saved anything.

So, does this mean that buying long term care insurance for parents is worth it?

Yes, it is worth it to buy long term care insurance for elderly parents before it is needed. The absence of a long term care insurance policy will make it hard or worse impossible for your aging parents to pay for home care, nursing home, assisted living facilities and others.

To further understand insurance for long term care, here are quick facts that you should know or you can visit our FAQs page.

What is Long Term Care Insurance?

Long term care insurance is a type of policy that pays for different types of long term care services and facilities such as home care, nursing home, assisted living facilities, adult day care, and others that an individual might need because of old age, illnesses or injury.

How does Long Term Care Insurance Work?

A long term care insurance policy starts paying for benefits when the policyholder trigger the benefits or qualifying events or when the elimination period expires.

Benefits can be triggered when an individual can no longer perform two or more of the six ADLs or has a cognitive impairment like Alzheimer’s or Dementia.

Elimination period or the length of time that must pass after triggering the benefits before a long term care policy starts paying for benefits.

How Much Does Long Term Care Insurance Cost?

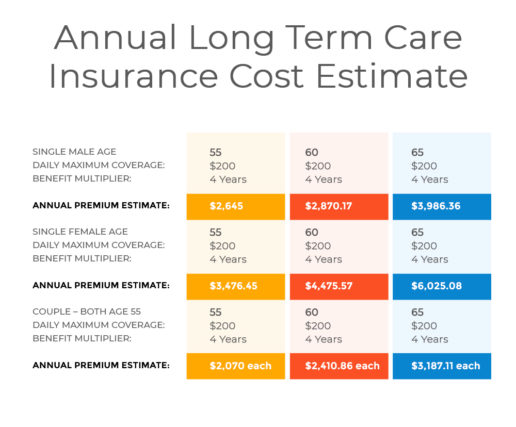

The cost of long term care insurance depends on the policyholder’s age, health, gender and policy features. It’s best to purchase a policy when an individual is young and healthy to avail of health discounts of up to 10%. Insurance providers favor these potential policyholders since they are healthy and will less likely file for claims.

Here are the estimate costs of long term care insurance for men, women, and couples

Reasons Buying Long Term Care Insurance for Parents is Wise

1. Health Crisis

No one knows what the future holds. You’re aging parents might be in fine fettle today but what about tomorrow, will they still have the same vigor, energy, and good health?

Don’t let this cloud of uncertainty go unnoticed since aging individuals are vulnerable to illnesses and injuries that might require expensive long term care supports and services.

In case your elderly parents would need assistance in carrying out their six Activities of Daily Living (ADLs) such as eating, bathing, toileting, transferring, incontinence after a health crisis and you lack resources, a long term care insurance policy can pay for this.

Read Next: 6 Tips to Avoid $280,000 Health Care Costs in Retirement that Works

2. Expensive Long Term Care Cost

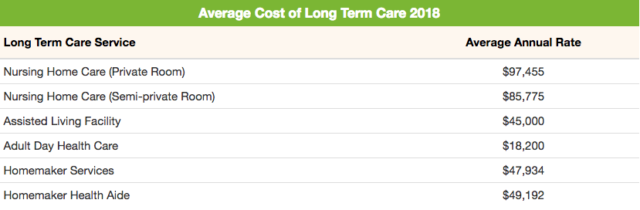

Did you know that your parents would need around $100,375 annually for a private room in a nursing home in the U.S? That’s just for this year since the rate is estimated to jump to $103,386 annually.

Here are annual median rates of other types of long term care facilities.

If your parents belong to the highest-income bracket then they can pay for long term care costs on their own. If they are a part of the lowest-income group, they can apply for Medicaid benefits that are limited. If they belong to the middle-income group, it’s a wise decision to have an insurance that will pay for their future care needs.

Related: Top 10 States with Cheapest Long Term Care in the United States: Map Infographic

3. Secure your Parents’ Future

There are still some individuals who mistakenly believe that Medicare can cover their long term care needs and because of this misconception 1 out of 3 Americans in their 40s haven’t planned for long term care.

It’s about time that people realize that this is just a long term care myth and they should purchase long term care coverage. Having coverage can secure your parent’s future by helping them age in a way they want and by giving them more liberty of choosing the care and facility.

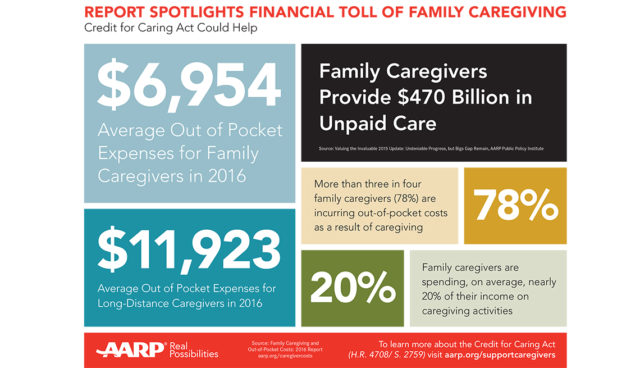

4. Financial Toll of Family Caregiving

The United States has roughly 40 million unpaid caregivers that use a big part of their savings to pay for the care needs of their loved ones. According to a study by AARP, these unpaid caregivers are spending around $6,954 annually, which is equivalent to 20% of their income.

Family caregivers will most likely dip into their savings, cut back on their personal expenses, save less for their retirement or worse, to take out loans. Female family caregivers are most affected since they are expected to take care of aging family members. They spend more hours at home taking care of loved ones and spend less time at work, which clearly jeopardizes their careers and savings for retirement.

Read: How Can You Ease Financial Burden of Caregiving to Women?

Do You Think It’s a Good Idea to Buy Long Term Care Policy for Aging Parents?

Given the current situation that more people are growing older and will most likely require long term care plus your financial security on the line, do you think it’s worth it to buy long term care insurance for your parents or not? Share in the comments below.