Family caregiving can be deeply fulfilling as family members are drawn closer together. However, as time goes by and the demands increases, unpaid family members have to make life-changing sacrifices such as financial, health and social needs, according to a survey conducted by Associated Press-NORC Center for Public Affairs Research.

Among family caregivers today, around 70% said they believe they are responsible for taking care of a family member, but 70% are worried that they might not be able to provide adequate care. Women who answered the surveyed are significantly more likely than men to believe that they will be responsible for family caregiving. All these findings are based from Lincoln Financial Group’s latest study.

Women as primary caregivers are typical in the long term care setting in the United States nowadays.

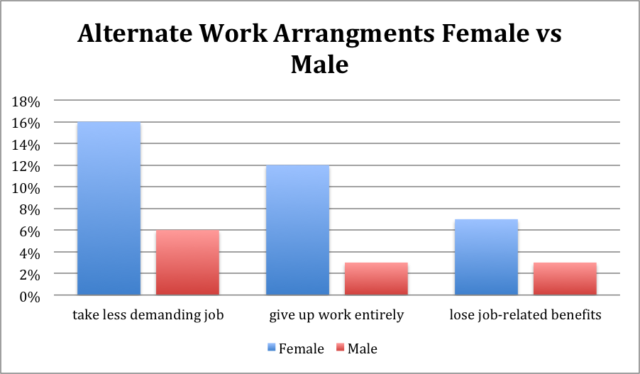

Yes, there are male caregivers but female primary caregivers spend as much as 50% more time providing care compared to their counterparts. This only means one thing, female caregivers are spending less time at work, which is alarming.

Women as primary caregivers have to make work adjustments such as these:

You surely don’t want to become a financial burden to your daughters, right?

So, here are ways you can alleviate the burden of caregiving on women.

1. Plan Early

It’s a very difficult time when it’s time for a loved one to receive care especially to female adult children who are expected to step in and take the role of caregiver unless you’ve prepared for this day to come.

Planning for long term care early is essential and yet it is often overlooked because of several long term care misconceptions like Medicare would pay for long term care or as bold as there’s only a slim chance you’ll require care. The truth is, Medicare doesn’t pay for long term care and around 70% of Americans 65 and above will need some form of long term care in the future.

Failure to plan for long term care can lead to outliving your assets and becoming a financial burden to your family. It’s best to understand long term care through helpful statistics, tools, and resources, be familiar with different types of supports and services available in your community and by exploring all the available options you have while you still have time.

Read Next: 5 Reasons Why Women Need Long Term Care Planning the Most

2. Government Programs

Are there really government programs that pay for long term care?

Yes, through Medicaid and Veterans Affairs Aid and Attendance.

Medicaid

It helps pay for long term care but you need to become eligible for benefits first and that means meeting the financial requirements required by the state you live in. Medicaid eligibility varies but usually, older Americans can’t have more than $2,000 in liquid in assets in order to qualify.

But there are drawbacks, not all long term care facilities accept Medicaid and only traditional nursing home is covered. So, assisted living is not an option.

Veterans Affairs Benefits

This pays for long term care supports and services for service-related disabilities as well as home care and nursing home for aging veterans who need long term care. It also pays for veterans who can’t pay for care.

Here are two VA programs to help veterans stay at home.

- The Housebound Aid and Attendance Allowance Program – This type of program gives to eligible veterans with disabilities and their surviving spouses to pay for home care or community-based long term care.

- Veteran Directed Home and Community Based Services Program (VD-HCBS) – This type of program started in 2008 for eligible veterans that provide veterans with a flexible budget to pay for services.

3. Buy Long Term Care Insurance Policy

Long term care insurance is an insurance product that helps fund for long term care services and settings that they need in the event of injury, accident, illness and old age.

Since the cost of long term care is skyrocketing today, it is best to buy long term care policy that can pay for home care, nursing home, assisted living, adult day care and more. Aside from it provides comprehensive coverage, it also gives peace of mind and protects your loved ones from the financial and emotional burden of long term care.

It’s recommended to buy long term care insurance as early as you turn 50 to make the most of health discounts, affordable premiums and to make sure that your long term care insurance application will not be denied. It’s recommended to shop around and request for free quotes to compare policies first and find the right one for your needs.

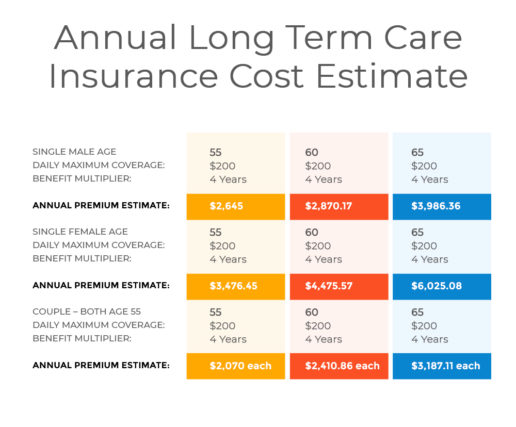

For your reference, here are estimate costs of long term care insurance.

Related: 5 Tips to Qualify for Long Term Care Insurance

4. Explore Alternatives to Long Term Care Insurance

In case you failed to buy long term care insurance and it’s too late or too expensive for you to buy coverage, here are long term care insurance alternatives you can consider.

Self-insuring

It helps you avoid paying for premiums that might end up unused, which you can use to pay for other things like to leave a legacy to your family, bills, travels, and others. However, self-insuring can be risky considering that the cost of long term care is rising. Right now, the average out-of-pocket long term care cost can go as high as $100,000 annually. But take note that health care cost is not yet included here, which is around $280,000 for a retired couple.

If you have assets worth over $2.5 million dollars and you live in a state that offers cheap long term care services and facilities, then you can consider self-insuring.

Hybrid Policy

Also known as life insurance with long term care rider is a type of policy that provides both death benefits and long term care benefits. It deserves a second look because it provides solutions to issues such as premium hikes and paying for premiums that an individual might not use. Also, it is perfect for individuals who have been delinked for long term care insurance.

But you should look the other way if you are at high risk of needing long term care since a hybrid policy provides limited long term care benefit. You might end up paying out-of-the-pocket care expenses that can drain your savings.

Short-term Care Insurance

As the name implies is an insurance that provides coverage for a short period of time. Short-term care insurance pays for home care, adult day care, assisted living, nursing home, and others for a few days up to 365 days. It is very appealing since it is less expensive, it has loose underwriting and the policy benefits take effect immediately. However, you might end up paying out-of-the-pocket costs since it only pays for care for a short period of time.

Group Long Term Care Insurance

Group long term care insurance or employer-sponsored long term care policy is perfect for individuals who can no longer buy traditional long term care policy since it has a simplified underwriting. It is also cheaper and offers unisex rates. But it only covers 50%-75% of home care, unlike traditional long term care insurance that pays for 100% home care.

5. Consider Adult Day Care

Adult day care perfect for care recipients with family caregivers who need to go to work. This type of care is used to relieve the family caregiver her duties and to ensure that her loved ones will still receive quality care even if she is at work.

Instead of forcing your loved one to make adjustments to their work just to take care of you, you can consider going to an adult day care so your loved one can continue working.

Conclusion

Failing to plan for your future long term care needs has negative effects on your loved ones particularly to your female children since they are expected to become your caregiver. If you want to spare your daughters from the financial burden of family caregiving then you should prepare for your care needs as early as possible and determine the best payment long term care option perfect for your needs be it a traditional long term care policy, hybrid insurance, self-insuring or others.