Let ALTCP help you find the best long term care insurance perfect for your future long term care needs by requesting for no-obligation quotes now.

Short term care insurance is taking the insurance market by storm. But does it offer real value to policyholders and can be considered as a substitute to long term care insurance?

Let’s find out.

Long term care planning is essential nowadays since people are living much longer, which makes them at risk of needing long term care. Based on the latest ltc statistics, 70% of Americans 65 and above will receive care at home, in nursing homes, assisted living facilities and more.

However, some people are starting to think short term. They opt for short term care insurance as its name suggests, is a type of insurance that provides short coverage for long term care.

What is Short Term Care Insurance?

Short term care insurance is a type of insurance that helps pay for rehabilitation from injury, operation, disease and situations when a person needs assistance with their activities of daily living (ADLs) like eating, bathing, dressing and toileting. As the name implies, short term care insurance policy is designed to provide benefits for a few days up to 365 days.

What Does Short Term Care Insurance Cover?

Short term care coverage works similarly with long term care insurance. Generally, it covers home care, adult day care, assisted living facility, skilled nursing home and nursing home just like long term care coverage. But they differ on the length of coverage. The former provides benefits up to 1 year only compared to the latter that provides benefits for years.

You can start receiving benefits when you can no longer carry out at least two of the six ADLs – eating, bathing, toileting, dressing, transferring and continence or if you have a cognitive impairment such as Alzheimer’s or Dementia, which is similar to long term care insurance.

Why You Should Consider Getting Short Term Care Policy?

1. Less Expensive

The cost of a short term care policy is more affordable than long term care insurance. Short term care insurance cost is actually the biggest selling point of this insurance product. In fact, the estimate costs of this policy are as follows:

Age 65 – $105

Age 70 – $141

2. Policy Benefits Take Effect Immediately

A short term care policy can be considered as a straightforward policy since it the benefits take effect immediately most of the time. This type of policy pays benefits as early as your first day of qualifying for benefits unlike most long term care policies are sold with a 90-day elimination period, which means you need to wait for 90 days before your benefits are paid.

3. Loose Underwriting

Its underwriting standard is loose, which makes it attractive to those who are having a hard time qualifying for long term care insurance. With this lax underwriting, more applicants can qualify for coverage regardless of their age.

Check out our guidelines on How to Qualify for Long Term Care Insurance

Who Should Buy Short Term Care Insurance?

- If you didn’t qualify for long term care insurance

- You waited too long to purchase long term care policy and now your premiums are too high.

- You prefer a more affordable long term care coverage.

- You’re a single woman who wants a less expensive option.

- You already have long term care insurance but you want to cover your elimination period.

What is Long Term Care Insurance?

Long term care insurance is designed for individuals who need funds for their long term care needs to sustain their quality of life in the event that they can no longer do their activities of daily living (ADLs) including eating, bathing, toileting, dressing, transferring and continence.

Read Next: Complete Guide To Long Term Care Insurance

What is Covered by Long Term Care Insurance?

Long term care insurance policies cover different types of long term care services and settings including home health aide, home maker services, nursing homes, assisted living facilities, adult day care and CCRCs, which are known to be very expensive.

This type of policy is designed to help individuals protect their assets and loved ones from the devastating cost of long term care, gives peace of mind knowing that they will be covered for years and can also help relieve the burden of caregiving to family members, which is emotionally, physically and financially challenging.

Why You Should Consider Getting Long Term Care Insurance?

1. Protect your Assets

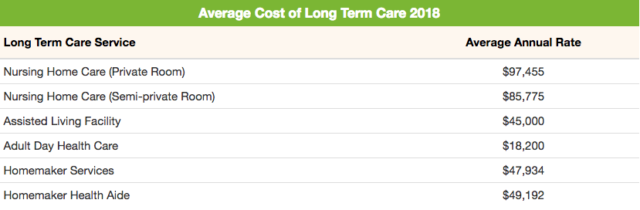

Long term care costs continue to skyrocket nowadays, which makes it hard for individuals to afford particularly those who would need care for an extended period of time.

The average costs of long term care by state today are as follows

While there are U.S states that affordable long term care options, this is not an excuse to plan early and shop for long term care insurance coverage.

2. Discounts on Premiums

Most people think that long term care insurance is outright expensive. The truth is, you can save money when buying long term care insurance through discounts given by insurers. If you buy coverage early like when you’re in your 50s, you’re eligible for up to 15% of preferred health discount. Couples who want to buy a policy are also entitled to a discount of up to 30%. But take note that these discounts are not cumulative and they vary by state.

Save up to 30% when you shop for long term care insurance now!

3. Relieve Burden of Caregiving on Family

There are around 43.5 million unpaid caregivers in the United States today. These family caregivers who are mostly women are negatively affected by providing care to their loved ones. It may be overwhelming but these numbers can’t hide the fact that caregivers suffer emotionally, physically and financially:

- 1 in 5 caregivers experiences high levels of physical strain.

- 1 in 5 caregivers experiences financial problems.

- 2 in 5 caregivers experience emotional stress.

- 3 in 5 working caregivers have experienced at least one impact in their employment situation.

Learn about 18 Enlightening Facts about Caregivers through our infographic

Who Should Buy Long Term Care Insurance?

- If you want to protect your assets and leave a legacy behind to your loved ones.

- You want to maintain your independence and uphold your dignity when the time comes you’ll need long term care.

- You want to protect your family from the devastating cost of care and caregiving duties.

- If you’re single and you want to make sure that you’re long term care needs will be met in the future.

- You have a family history of a chronic illness that would require care for an extended period of time.

Conclusion

Short term care insurance has its shining moments but based on the facts and stats presented above, it is clearly lacking in benefits that most aging Americans will require. Its selling point of being affordable and having lax underwriting can make some heads turn but the maximum long term care coverage of 1 year will make you think twice if this policy can offer real value.

It’s a good plan B if you can’t get traditional coverage for long term care. Having some insurance is still better than not having any insurance at all. But when you take into consideration the average length of stay of older individuals in long term care facilities, which are 2 years and 2 months for men and 3 years and 7 months for women, long term care insurance policies give more value compared to having coverage for just a year or less. So, if you’re younger, healthier and you can afford it, shop for long term care insurance now.

This is a very informative article. As someone who knows first hand that a health crisis requiring short or long term care can surprise anyone at anytime, I have a greater appreciation for planning for the possibility of requiring caregiver services. This article clearly points out the differences between the two types of care policies.

Totally, agree! The key is to prepare for care needs to avoid financial mishaps such as paying for long term care expenses out-of-the-pocket, which is very costly. Also, it’s important to explore coverage options and choosing what would work perfectly for them.