Long term care insurance vs self-insuring is one of the issues that people consider before retiring. While some individuals choose to buy a traditional long term care insurance policy, some might get more advantages out of self-insurance.

Traditional Long Term Care Insurance vs Self-insuring

Self-insurance refers to funding the expenses of long term care through assets and other financial resources that a person owns. One method of self-insurance is accumulating savings and later using this saved money for long term care expenses, including buying medications or paying caregiver service fees.

In fact, paying out-of-pocket is advisable for people whose assets, including the home, are worth over $2.5 million. Self-insuring can be effective in states with relatively low costs of skilled nursing care, assisted living, and home health care. Wealthy individuals who live in certain areas with more affordable long term care can also consider this approach.

An obvious advantage with self-insuring is avoiding the expenditure for premiums that might end up unused. For those who have excellent physical and cognitive health for the remainder of their lives, self-insurance is a way to ensure that the money that would end up in unused premiums can now be spent on inheritance, tuition, bills, and even post-retirement leisure. Moreover, those who are self-insured do not have to have a mandatory medical exam like those who are applying for a policy.

Premiums for long term care insurance have continued to rise over the years. Some insurers are planning to step up the value of premiums between 2% and 5% every year. Another concern is the survival of long term care insurance products on the market. These matters do not affect the people who choose to self-insure.

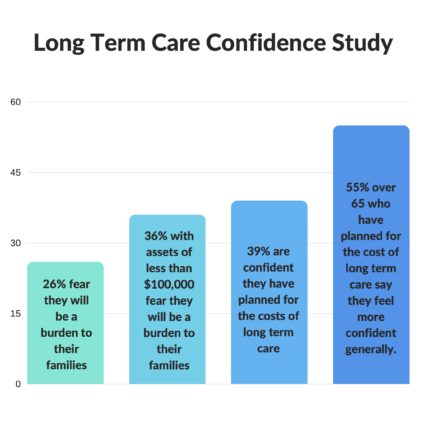

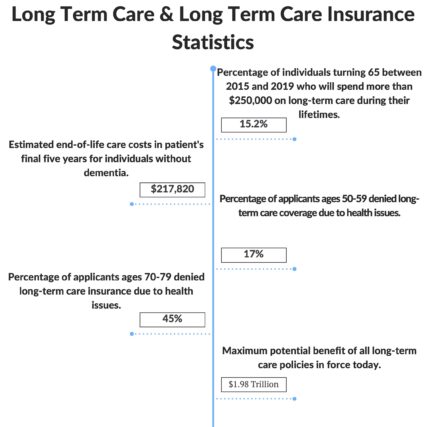

Must-Know Statistics on Long Term Care

To help ensure that you’re on the right path and make the best life-changing decision, here are some statistics that you can use as your reference:

credit: www.lfg.com

credit: www.morningstar.com

Read: Top 9 Long Term Care Facts and Statistics

Preparation Can Give the Upper Hand

Despite the benefits of self-insurance, affluent individuals might lose significant amounts of cash and become unable to keep up with this method after a long time. Long term care costs will continue to increase in the years to come due to inflation.

A traditional long term care insurance policy offers inflation protection so a client can amass even more money to a pool of insurance benefits. Riders, such as shared care, help policyholders manage their finances more effectively in various ways.

One of the most useful perks that a long term care insurance policy can give is preparedness. Saving more than enough money to pay for the costs of care takes time. People might suddenly experience an illness or injury that necessitates immediate long term care. Such events also hinder them from earning income. Policyholders, on the other hand, receive coverage for the duration of their benefit period.

A traditional long term care insurance policy is recommended for people who have insufficient assets for self-insurance but lack the eligibility for government-sponsored long term care programs.

When exploring your options to either self-insure or purchase LTC insurance, know that a Health Savings Account can play an extraordinary role in helping cover your long-term care expenses. In fact, HSAs offer a trifecta of tax benefits that make it the most tax-efficient savings vehicle available! As long as you qualify to fund an HSA, you can save pre-tax dollars into an HSA and use those dollars to pay for qualified medical expenses – which includes long term care costs AND long term care insurance premiums.

Read: LTC Insurance: Definition, Costs, and Policy Details

Compromise between Two Options

Those who are still deciding whether to self-insure or buy traditional long term care insurance may want to consider a combination of these two options. This compromise involves paying for adequate – but not full – long term care coverage that costs less. After that, a person shifts to self-insurance. An example is buying a policy with three years of the benefit period, and then paying out-of-pocket when that period is over.

Reversing this approach works for some people. They shoulder care expenses for a few years before relying on long term care insurance benefits.

Before making a decision, be sure to keep this advice in mind and choose the option that works best for your specific financial situation and your future long term care needs.

One thought on “Long Term Care Insurance vs Self-Insuring: What Is Best for You?”