There’s a 70% chance that Americans will move to a long-term care facility such as an assisted living facility or nursing home when they turn 65. Despite this report by the U.S Department of Health, most individuals still put off preparing for the high cost of assisted living.

According to ALTCP long-term care cost, the annual median cost of assisted living is $46,350. Without a proper plan in place like massive retirement savings or insurance, you might end up spending a huge chunk of your savings or worse, you’ll become a financial burden to your loved ones. Although there are some U.S states that offer affordable assisted living facilities, it’s not an excuse to stall planning for their future long-term care needs.

To help you get started, here are different ways you can pay for assisted living costs.

1. Long-term care insurance

Long-term care insurance is defined as an insurance that helps fund long term care supports and services that include assisted living facility. Unfortunately, only 7.2 million Americans have coverage for long-term care out of around 46,790,727 million individuals 65 and up who are at risk of requiring any form of long-term care.

This type of policy can address the gap left by Medicare and Medicaid since these government programs don’t pay for everything. You might end up paying out-of-the-pocket, which can derail your retirement plans. So, if you don’t have a policy yet, now is the best time to buy a policy. It’s recommended to shop long-term care insurance early to avoid paying high premiums and being declined for coverage.

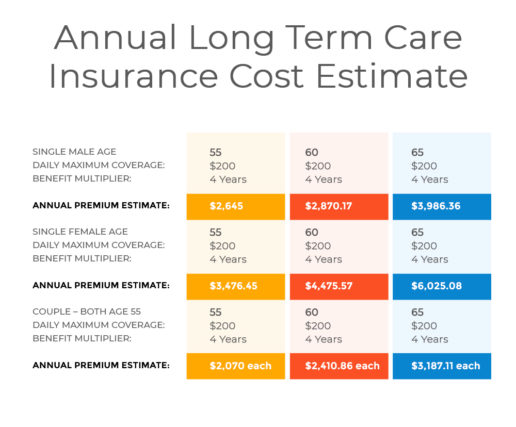

Here are estimate costs of long-term care insurance by age, which you can use to help you come up with a well-informed decision.

2. Out-of-the-pocket

Paying out-of-the-pocket or using your savings is the easiest way to pay for assisted living expenses. However, it’s the riskiest too. You might end up outliving your assets if you use your savings or retirement income considering that assisted living is costly. To make things worse, you might become a financial liability to your loved ones. This should be the last option on your list.

3. Life Insurance

Life insurance is known as a policy that only takes effect when the policyholder dies. Well, that’s not the only way life insurance works. In fact, this type of insurance can provide financial support in any way you need like paying for your long-term care needs.

One way to receive financial support from life insurance is by cashing it out. It works this way, your insurer will buy your policy back for 50% to 75% of its value. However, the rules in cashing out policies vary depending on the company and the type of policy you have. There are some instances wherein the policy can only be cashed in if the policyholder is terminally ill.

Another option is through 1035 exchange or repurposing your old life insurance and turning it to long-term care insurance. The conversion of life insurance pays 15% to 50% of the value of your life insurance. It is less then life settlement or cashing out your policy but it’s a great option if you have a lesser-value policy that might not be eligible for life settlement.

Related: 1035 Exchange: Trading Your Life Insurance to Long-Term Care Insurance

4. Veterans Aid & Attendance Program

Veterans Aid is a program that is generous in providing help to those who have served the country. If you or your loved one is a veteran, you might be eligible for benefits that can pay for long-term care.

This type of pension typically pays up to $1,830 per month to a veteran, $1,176 to a surviving spouse or $2,170 per month to veteran couples and surviving spouses. However, your eligibility depends on income and assets limit set by the Veterans program.

You can keep more assets in Veterans Aid & Attendance Program compared to other state aid programs, and it also provides a higher level of assistance. But, you cannot receive benefits from both programs so evaluate these programs first before choosing what can provide more assistance to you or your loved one.

5. Medicaid

Medicaid is a government program that pays for long-term care facilities and services. But in order to qualify for this program, you need to have assets and income that are below poverty level. Your assets should be less than $2,000 before you can qualify for Medicaid benefits. But take note that Medicaid eligibility requirements vary from one state to another so it’s best to verify this to your Medicaid state office first.

6. Reverse Mortgage

A reverse mortgage allows you to borrow money based on your home’s equity, which you can pay when you move out or sell the home. You can use the money to fund your assisted living expenses.

This is a good option for individuals who are uninsurable and they have assets that make them ineligible for Medicaid benefits. However, this is not a wise idea if you prefer to keep your home within your family.

7. Annuity

If you have big savings and you’re worried that you might outlive your assets, then you should consider annuity. An annuity can provide you with regular payments over a specific period of time in exchange for the lump sum you paid to the underwriters.

This is a clever way of stretching your money and making sure that you will have a steady flow of income even if you live longer than you expected. Another thing that makes annuity beneficial is that Medicaid doesn’t consider it as an asset in case you apply for this government program since it is considered a resource.

Take Away

Which among these assisted living payment options you think would work best for you?

Just keep in mind that what works best for others might not work for you. It’s best to understand each of these options and find out what can give you and your family optimum protection from expensive cost of assisted living facilities.

If you want to know more about long-term care insurance, our long-term care specialist will provide you one-on-one guidance in choosing the best policy that targets your care needs and can help you avoid overspending on your policy by giving you free quotes.