Have ready are you for retirement? If you’re a woman, your future seems bright since women are known to more likely prioritize financial planning compared to men.

Despite women being better planners, they still end up feeling they’re not ready for retirement. In fact, 40% of women revealed that they don’t have enough money saved for retirement. How is this possible when women know the secret ingredients to a successful retirement?

Unfortunately, women face more retirement challenges than their male counterparts, which make them feel less prepared for retirement.

To help women get ready for retirement, we’re featuring five articles that highlight unique challenges on women’s retirement and how to manage them.

Long Term Care Is A Woman’s Issue

The title says it all, long term care is one of the biggest retirement issues women face today. According to The Atlas Approach’s article, women are more likely to outlive their spouse or partner, step up as the family caregiver to their loved ones and require long term care needs for an extended period of time.

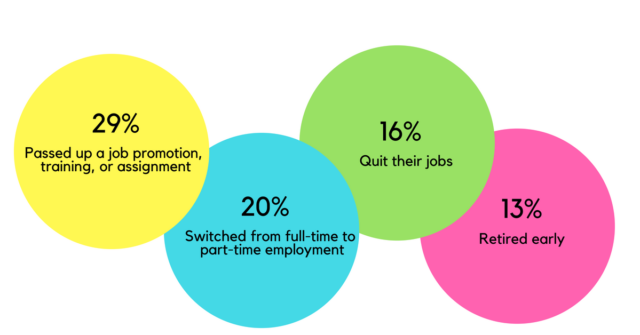

Since women are considered as the nation’s caregivers, they experience conflicting demands of work and long term care. They spend less time working, pass up a job promotion, quit their jobs or retire early because of their demanding caregiving duty.

Caregiving will have a financial toll on family caregivers since they’ll spend an average of for out-of-pocket care costs. These challenges make it hard for women to get ready for retirement but not impossible.

Some steps that women can do to address their potential care needs is by maintaining good health, anticipating their future, planning for long term care as a family and by considering insurance.

Read: 5 Reasons Why Women Need Long Term Care Planning the Most

OPINION: Gender Pay Gap – Statistics, Trends, Reasons and Solutions

Women earn about 79 cents per dollar compared with white men. The gender pay gap gets worse for women of color compared to white men. Hispanic women are paid just 54.4 cents on the dollar while African American women are paid 62.5 cents on the dollar.

So, what causes the gender pay gap?

Here are some factors that contribute to inequality:

- Family Responsibilities – Women are more likely than men to take some time off from work to take care of children or their aging loved ones. This time off reduces women’s income.

- Discrimination – Some companies have discrimination in hiring and wage-setting practices.

- Job Choices – Women often do jobs in lower-wage industries and those that are traditionally feminine like taking care of children and seniors.

- Different Hours: Women work about 35 minutes less per day than men.

- Negotiation – Women are less likely than men to negotiate their starting salary or raises, which can be a huge factor in the wage gap in higher-earning departments.

What can women do to get equal pay?

- Discuss salary and compensation.

- Advocate for better parental leave policies.

- Vote for representatives pursuing policies on equal pay.

- Encourage others to participate.

- Evaluate your own company.

- Advocate for all women.

Stakes are Higher for Women When Claiming Social Security

The retirement benefits you receive from Social Security is based on your work record. Since women spend most of their time out of the workforce to take care of their children, spouses or aging loved ones their earning records decreases, which also means their Social Security benefits decrease.

According to CNBC, women are clearly facing an uphill battle when claiming Social Security and planning for retirement because of unique challenges such as longevity and they spend more years in retirement.

Once they are retired, women have unrealistic expectations from Social Security. Around 58% of women expect Social Security to cover all their retirement expenses. The truth is, only around 40% of their expenses will be covered.

To avoid coming up short in retirement, women should start strategizing early, avoid making claims at 62, consider the consequences of divorce or death of a spouse and seek a professional opinion.

The Trickle-Down Effect of Caregiving on Women

There are about 40 million caregivers today and 60% are women. Their decision to take the responsibility of providing care to their aging family member has major repercussions to their retirement.

The trickle-down effect of caregiving to women affects their ability to save for retirement and take care of their own health. Instead of staying in the workforce, women choose to quit their jobs because of the psychic and financial toll of caregiving.

According to Aparna Mathur, of the American Enterprise Institute, policies that support paid family leave could make it more likely for women to go back to their jobs and continue pursuing their careers instead of quitting.

Another key finding of the conference is the massive effect of a 60-something woman who stops working sooner than expected takes herself out of any employer-sponsored retirement savings plan, which according to Kathleen Kennedy Townsend, director of Retirement Security at the Economic Policy Institute is the most effective method for saving for retirement.

Related: Family Caregivers: The Everyday Superheros

18 Findings on Women and Retirement: New Survey Shows Hardships That Women Face

One of the challenges that women face today is their lack of financial knowledge or education. The article by CBN News revealed that women expect to need $500,000 in retirement but 55% admitted that it’s just a guess. Around 47% of female baby boomers know quite a bit or a great deal about Social Security benefits.

Seeking professional help can help women improve their financial literacy. Sad to say, only one-third of women use professional assistance when planning for retirement.

Conclusion

Women will most likely take the rough road when planning for retirement. It’s tough but having a successful retirement is not an impossible feat. Women need to be proactive with their retirement plan by addressing issues like effects of family caregiving, longevity, needing long term care for an extended period of time, gender pay gap and other unique retirement issues.

It’s time for women to step up not for other people but for themselves.