What’s the first thing that comes to mind when you think of long term care insurance?

Expensive? Nursing home? A policy you won’t need?

People have their own interpretations of a long term care policy. Having these misconceptions around, most consumers come up with negative thoughts about this policy and can prevent them from knowing what long term care insurance can really bring on the table.

To help you understand this policy more, here are long term care insurance facts that can provide long term care solutions you and your family need.

1. You Decide Where to Receive Care

Most people think that long term care insurance pays for nursing home only. It pays for different types of long term care services and facilities such as assisted living, adult day care, and home care.

This perfectly suits around 77% of older adults who prefer to receive care at home. Based on recent statistics, more than half of new long term care insurance claims were for people who received care at home.

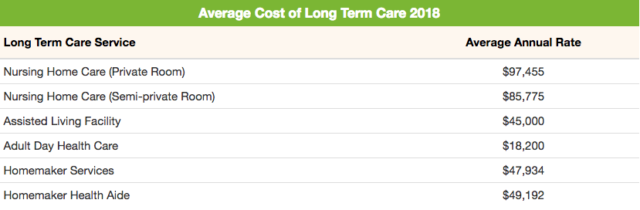

According to ALTCP’s long term care cost, the cost of homemaker services is $135 per day and $4,114 per month. The cost of a home health aide is $139 per day and $4,222 per month.

Those who don’t choose home care will have to pay these rates:

2. Tax Deductible

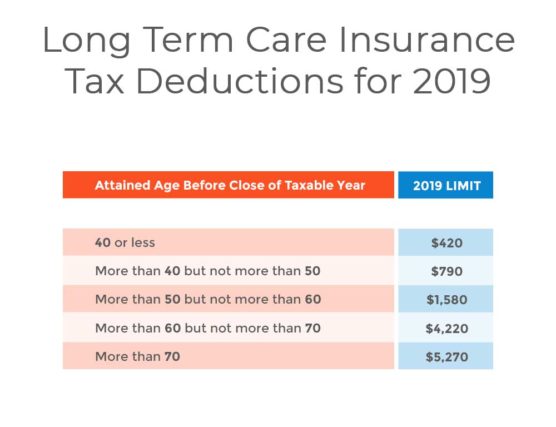

The federal government gives tax deductions as incentives to individuals who have qualified long term care policies. This is their way to encourage individuals to buy coverage for their future long term care needs and to lighten the burden of Medicaid from paying long term care expenses.

But take note that long term care insurance tax deductions have limits that are based on the policyholder’s age at the end of the taxable year. Below is the tax deductions for 2019.

Read Next: Long Term Care Tax Deductions

3. Supports Family Caregivers

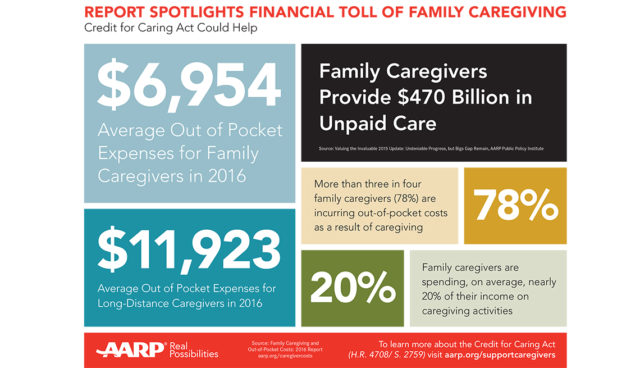

Buying long term care insurance is not limited to protecting your assets but it’s also a way to support family caregivers. There are approximately 34.2 million caregivers that provide unpaid care to an adult 50 years old and above. They feel that they don’t have any choice but to accept the caregiving responsibility even if they have other responsibilities such as their job, taking care of their children and saving for their future.

Around 70% of family caregivers experience work-related difficulties because they juggle work and caregiving duties. They end up spending less time working and earning less. But that’s not even the worst yet. AARP’s report on the financial toll of family caregiving showed that family caregivers spend an average out of pocket expenses of $6,954.

Most long term care insurance policies recognize family caregivers and allow their services to be reimbursed through the policy.

Related: How Family Caregivers Can Keep Up with the Emotional and Financial Toll of Caregiving

4. Shared care

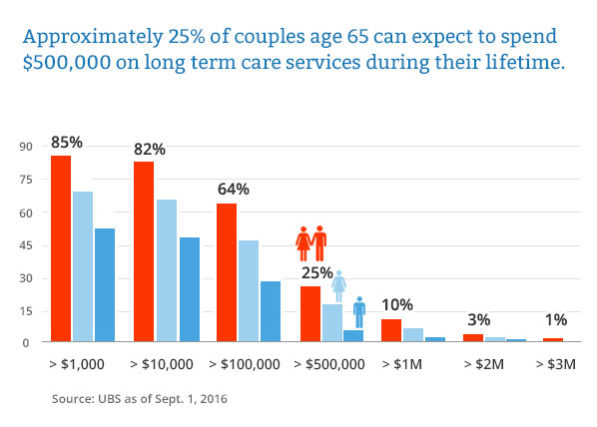

You and your spouse don’t need two policies to have coverage for long term care. Its cost continues to rise, which is starting to raise concerns for couples. In fact, there are around 25% of couples that are 65 years old and above who can expect to spend $500,000 on long term care.

Through the shared care policy feature, you and your spouse – married or not – can access coverage that is enough for two people. This rider combines the benefits into a pool that can be accessed by both.

5. Survivor waiver of premiums

A survivor waiver of premiums is designed to protect the surviving spouse from paying premium payments. This is beneficial to individuals who have spouses that are the primary wage earner. Without this benefit, a surviving spouse will have a hard time keeping up paying for the premiums and might end up dropping the policy.

Some policies have the option to add a seven-year survivorship benefit or 10-Year survivorship benefit.. The carrier will permanently waive the premium for the surviving spouse or partner for 7 or 10 years when the other spouse or partner dies.

In case your relationship ends because of divorce or final separation, remember to terminate this benefit.

6. Inflation Protection

Adding inflation protection rider to your long term care insurance is an absolute must even if that means increasing your premiums. Inflation protection allows your policy to keep up with the rising cost of long term care, which decreases the chance of paying out-of-the-pocket.

Here are the three types of inflation protection:

Simple Inflation

Increases the daily benefit by 5% every year. The policyholder’s daily benefits will double by the 19th year and a half. But take note that premiums will increase by 40% to 60% if you avail of this rider.

Compound Inflation

This kind of rider is more beneficial to younger and healthier individuals according to experts. Compound inflation increases the daily benefit by 3% to 5% compounded annually.

Guarantee Purchase Option/Future Purchase

Allows the policyholders to increase their daily benefit every two to three years without facing additional underwriting. However, this is expensive since each new offer is based on the current age of the policyholder.

7. Return of Premium Benefit

One of the reasons why people don’t purchase long term care insurance is because they’re afraid they’ll buy something they will never use. If this is your primary concern, you should consider the return of premium benefit.

There are carriers that provide the option to add a return of premium benefit to your policy. When you pass away, the carrier will pay your heirs all your premium payments, less all the benefits paid against the policy.

8. Non-forfeiture Benefit

This is designed to ensure that in case you lapse your policy after a certain number of years, you retain some benefits of your policy.

Here are the two types of nonforfeiture benefits:

Reduced Paid-Up Benefit

If you lapse your policy after a specific number of years, your will policy will continue with reduced daily benefit amounts. However, there are some carriers that only apply this benefit to nursing home benefits.

Shortened Benefit Period

After your lapse your policy for a specific number of years, your policy will continue to cover the same benefits that would have been covered by your policy until exhausting your nonforfeiture benefit amount.

9. Restoration of Benefits

This long term care insurance benefit is designed to restore your benefits after receiving benefits from your pool of money. This is suitable for policyholders who will file for one expensive claim one after another.

Conclusion

These facts about long term care insurance can help you understand how this policy works and how policy features can help you maximize your coverage is the key to securing your future and protecting your loved ones.

If you’re ready to explore your options, request for a free quote now. We’ll help you save time and money by shopping the market for you and finding you the best available policy based on your needs.